Silver

Silver Gold

Gold Platinum

Platinum Palladium

Palladium Bitcoin

Bitcoin Ethereum

EthereumGold IRA Rollover: Step-by-Step Guide (2026 Update)

Disclosure: We are reader-supported. If you purchase from a link on our site, we may earn a commission. Learn more

BY J.B. Maverick

- UPDATED: March 18, 2026With gold prices elevated in 2026, many American investors are looking into ways to add physical gold to their retirement accounts. Investing in gold through an IRA generally involves a gold IRA rollover, a transfer, or a cash contribution. In this guide, we’ll walk through how a gold IRA rollover works, how it compares to a transfer, and what investors should know before opening a self-directed precious metals IRA.

Table of Contents

- Get Noble Gold’s Free 2026 Gold IRA Kit

- Top Rated Gold IRA Rollover/Transfer Companies

- Gold IRA Rollover: The Quick Answer

- What is a Gold IRA Rollover?

- Gold IRA Rollover vs. Gold IRA Transfer

- 401(k) to Gold IRA Rollover

- Deciding on a Gold IRA Rollover Strategy

- Gold IRA Rollover: Choose IRS-Approved Bullion Bars

- Gold IRA Rules and Contribution Limits

- Physical Gold IRA Rollover vs. “Paper Gold” Rollover

- Finding the Best Gold IRA Custodian

- List of Top Gold IRA Companies

- Eligible Account Types for a Gold IRA Rollover

- Gold IRA Rollover FAQs

- Are You Ready to Start Your Rollover?

Get Noble Gold’s Free 2026 Gold IRA Kit

Want a simple walkthrough before you move retirement funds? This free kit covers rollover basics, common fee traps, and the questions to ask before opening a metals IRA.

Disclosure: We may earn a commission from some partners featured on this page. This guide is for informational purposes only and is not financial, tax, or legal advice.

Top Rated Gold IRA Rollover/Transfer Companies

Noble Gold

A strong all-around choice for investors who want a well-known gold IRA provider with a straightforward onboarding process, solid educational materials, and broad mainstream appeal.

GoldenCrest Metals

A solid option for investors who want more flexibility around coin and bullion choices and prefer working with a provider that emphasizes product selection.

Augusta Precious Metals

Often favored by investors who want a more consultative feel, more hand-holding during the rollover process, and a service model that tends to appeal to larger account sizes.

To simplify the process, we’ve put together this short guide to gold IRA rollovers. In most cases, you’re moving retirement funds rather than transferring stocks or ETFs as-is into a physical metals IRA. Those funds are typically moved into a self-directed account and then used to buy IRS-approved bullion inside a tax-advantaged retirement account such as a self-directed Roth or Traditional IRA.

Gold IRA Rollover: The Quick Answer

A gold IRA rollover is the process of moving eligible retirement funds into a self-directed IRA that can hold IRS-approved physical gold and other qualifying precious metals.

In many cases, a direct rollover or trustee-to-trustee transfer is cleaner than an indirect rollover because it reduces timing mistakes and withholding issues.

If the money is paid to you first, you generally have 60 days to complete the rollover properly or you could trigger taxes and possibly penalties.

Before funding, confirm all-in fees, storage rules, custodian quality, and whether the metals you are buying are clearly IRA-eligible.

Bottom line: many investors prefer a direct movement of retirement funds into a self-directed IRA because it is usually cleaner and easier to manage than taking possession of the funds first.

What is a Gold IRA Rollover?

Gold IRA Rollover in 5 Simple Steps

- Confirm eligibility: old 401(k) plans are usually easiest; current-employer plans may require an in-service rollover or have restrictions.

- Open a self-directed IRA: choose a custodian that supports physical precious metals and works with an approved depository.

- Choose the safer funding method: prefer a direct rollover (401(k) → IRA) or trustee-to-trustee transfer (IRA → IRA) when possible.

- Select IRS-approved bullion: stick to widely recognized products that meet IRS requirements and avoid collectibles.

- Review the total cost: confirm setup fees, annual fees, storage, insurance, and buy/sell spreads before you fund.

A gold IRA rollover describes moving retirement funds from an existing account, for example a 401(k), Roth IRA, or SEP IRA, into a self-directed IRA, then using those funds to purchase IRS-approved bullion such as qualifying coins or bars inside the account.

In short, a gold IRA allows you to own real physical precious metals in your retirement account on a tax-deferred or tax-free basis. A gold IRA rollover is the process that allows you to create and fund such an account by moving eligible assets or cash from an existing retirement account.

During an indirect rollover, funds are withdrawn from the existing account and must be redeposited into the new IRA within 60 days. If taxes are withheld from the distribution, which is common with employer plans, you generally must deposit the full amount of the distribution, including the withheld portion using other funds if necessary, to avoid that amount being treated as taxable.

Gold IRA Rollover vs. Gold IRA Transfer

Investors have two main ways to fund a gold IRA: a rollover or a transfer. A transfer is often the more secure and lower-friction option for moving money between retirement accounts because the funds move directly between custodians. A rollover can still work perfectly well, but it comes with more rules if the money is paid to you first.

Below, we’ve listed some of the key differences between gold IRA transfers and rollovers as well as certain core similarities.

Gold IRA Transfer Rules | Gold IRA Rollover Rules |

|---|---|

| No 60-day transfer rule in effect | 60-day transfer rule applies, in which the account holder must transfer the deposited funds from their account into the new gold IRA |

| No early withdrawal penalties | distributed funds are subject to a 10% early withdrawal penalty if the account holder is under the minimum withdrawal age of 59.5 |

| Not taxable | If the 60-day rule is violated, the distributed funds are then deemed taxable as ordinary income |

| No annual limits | IRA holders are strictly limited to one rollover per 365-day calendar year |

| No withholding taxes | There is no tax withholding if a rollover is made from a personal IRA to another IRA |

A gold IRA transfer, sometimes referred to as an IRA gold transfer, involves moving funds from custodian to custodian. The account holder does not receive the money personally. Instead, the assets are moved directly between the institutions handling the retirement accounts.

The key difference between rollovers and transfers is that, in the case of IRA transfers, the distributed money never touches the IRA holder’s bank account. For more information about how the IRS regulates rollovers and what the consequences of violating the rules can be, see this IRS guide to general IRA rollovers and this broader IRS IRA FAQ.

For many investors, an IRA gold transfer is preferable because it reduces the chance of a costly error. In the case of an indirect rollover, it is possible to run into trouble by missing the 60-day deadline or misunderstanding the tax treatment of withheld funds. A direct transfer avoids much of that risk because the process is handled between custodians.

401(k) to Gold IRA Rollover

Despite what some investors believe, it is possible to transfer or rollover funds from an existing employer-sponsored or self-directed 401(k) to a gold IRA. That said, the process is subject to specific plan rules that should be checked before moving forward.

Rolling over funds from a 401(k) sponsored by a former employer into a new gold IRA is usually fairly straightforward. Simply choose a new gold IRA custodian and have them initiate the rollover on their end. A 401(k) sponsored by your current employer can be more restrictive.

If you’re rolling over from a 401(k) sponsored by your current employer, check the terms of your plan carefully. Some employer-sponsored 401(k)s do not allow precious-metals-related rollovers while you are still employed. Check your plan rules or ask your HR department or plan administrator whether in-service rollovers are allowed and what paperwork is required.

For a more detailed description of the process, check out our article on gold IRA rules and regulations. There you can find a broader guide to employer-sponsored 401(k) rollover considerations.

Deciding on a Gold IRA Rollover Strategy

There is no one-size-fits-all strategy. Your allocation should reflect your risk tolerance, time to retirement, and overall goals. If you decide to fund a gold IRA, many investors prefer a direct custodian-to-custodian transfer or rollover to help avoid unnecessary tax complications. It also makes sense to confirm all-in fees, including setup, annual administration, storage, and spreads, before committing.

Choosing Your Gold IRA Allocation

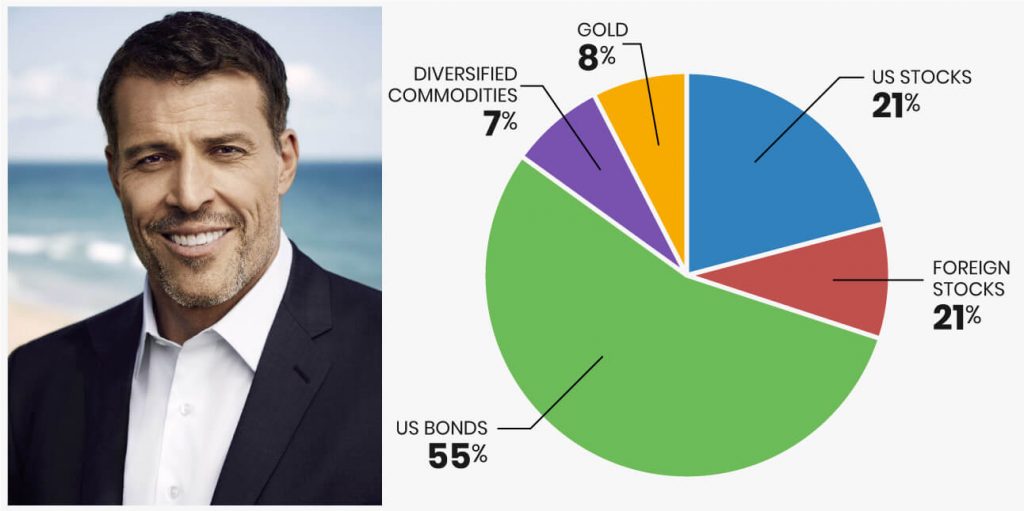

Some well-known investors and commentators have spoken publicly about keeping a portion of a portfolio in gold, but those examples should not be treated as a personal recommendation. Allocation decisions depend on your time horizon, risk tolerance, and overall retirement plan.

- What’s my outlook on the economy over the next 5 to 10 years?

- Has my portfolio been performing as expected over the past several years?

- What is my real reason for considering physical precious metals: diversification, inflation hedging, or something else?

- How close am I to retirement?

- Have I spoken to a qualified financial or tax professional?

For investors primarily focused on diversification, public discussions often mention a modest precious-metals allocation as an example. Investors more concerned with inflation or currency debasement sometimes lean somewhat higher. The more cautious approach is usually to think in terms of role and purpose rather than chasing an extreme allocation number.

Disclaimer: The content provided on this page and throughout this website is for informational purposes only. It does not constitute financial advice and should not be taken as such. Always speak to your financial advisor before making an investment decision.

Gold IRA Rollover: Choose IRS-Approved Bullion Bars

The IRS maintains strict standards regarding the type of gold assets that can be held within a tax-advantaged retirement account. For a complete list of authorized holdings, check out this guide to IRS-approved precious metals. These include, but aren’t limited to, the following types of gold assets:

In general, collectibles are prohibited from IRAs and 401(k)s under IRS rules, although there are exceptions for certain coins and qualifying bullion. A practical rule of thumb is to stick with widely recognized bullion products that clearly meet IRS requirements and that your custodian will confirm in writing as eligible before purchase.

- Certain coins described under 31 USC Section 5112

- Certain coins that fall under the IRS exceptions, including specific U.S. Mint coins and other qualifying coins described in the tax code

- Qualifying bullion of the required fineness, as long as a bank or IRS-approved nonbank trustee keeps physical possession, usually through an approved depository

Investing in unapproved assets may result in penalties or taxable treatment. To play it safe, many investors stick with straightforward bullion rather than rare or premium-priced collectible-style coinage. If you insist on investing in coins, review our list of top IRA-approved gold coins.

Gold IRA Rules and Contribution Limits

Gold IRAs follow the same general IRA rules as traditional IRAs that hold stocks and bonds. The main difference is the asset type, which in this case is physical bullion, along with the added custody and storage requirements.

One of the most important rules to understand is that account holders can only contribute a limited amount each year. For 2026, the annual IRA contribution limit is $7,500. If you’re age 50 or older, the catch-up amount is $1,100, for a total possible contribution of $8,600.

- Annual IRA contribution limit (2026): $7,500

- Annual catch-up contribution limit (2026): $1,100 for those age 50+

Importantly, there are also phase-out rules that some gold IRA investors must consider. These refer to the income thresholds that determine eligibility to make deductible contributions to certain IRAs. For 2026, the IRS lists the following phase-out ranges for deductible traditional IRA contributions when workplace retirement plan coverage is involved:

- For single taxpayers covered by a workplace retirement plan, the deduction phases out at a MAGI between $81,000 and $91,000.

- For married couples filing jointly where the spouse making the IRA contribution is covered by a workplace retirement plan, the deduction phases out at a MAGI between $129,000 and $149,000.

- For an IRA contributor who is not covered by a workplace retirement plan but married to someone who is, the deduction phases out at a MAGI between $242,000 and $252,000.

Note that overcontributing to your gold IRA can result in penalties. Overcontributed account holders may have to pay a 6% penalty on the excess contribution until it is corrected or absorbed by future contribution room. If that happens, this Fidelity guide on how to respond to an IRA overcontribution is a useful starting point.

Physical Gold IRA Rollover vs. “Paper Gold” Rollover

There are two main ways to get exposure to gold. First, there’s physical bullion, meaning actual bars or qualifying coins held in secure storage through an approved custodian. Second, there is “paper” gold, which can include securities such as gold mining stocks or ETFs.

Paper gold, like certain ETFs or mining stocks, and physical bullion can both play a role, but they behave differently. Mining stocks can be much more volatile because they are operating businesses with company-specific risks. Some gold ETFs are designed to track the spot price more closely, but they still come with fund mechanics, brokerage access, and fee considerations. Physical bullion is a more direct form of exposure to the metal itself, but it also comes with storage and custody costs, especially inside an IRA.

If you want to explore this further, see our guide on the advantages of physical gold versus securities-based gold exposure.

- Counterparty Risk: Unlike a publicly traded stock, a gold bar cannot declare bankruptcy. This can reduce certain forms of counterparty exposure compared with some paper-gold investments.

- Store of Value: Physical gold is often considered by investors looking for a tangible asset that may help diversify a portfolio.

- Direct Metal Exposure: Physical bullion inside an IRA gives investors exposure to the metal itself, though the metal must remain under approved custody rather than in personal storage.

- Distribution Flexibility: Gold can be distributed out of an IRA when the account holder chooses to take an in-kind distribution, subject to the normal tax rules that apply.

Although these benefits are not exclusive to precious metals, they are some of the main reasons why many investors consider holding gold as part of a broader portfolio.

Finding the Best Gold IRA Custodian

When you open a regular Traditional or Roth IRA, you can usually do it online through a mainstream brokerage. A physical gold IRA is more specialized because IRS rules require approved custody and storage for the metals.

Most mainstream brokerages, such as Fidelity or Charles Schwab, generally support paper gold products like certain ETFs inside standard IRAs, but physical precious-metals IRAs typically require a self-directed IRA custodian plus approved storage. To open a gold IRA, you have to research and select a gold IRA custodian. This is the company that will initiate and help facilitate your rollover or transfer with your current provider.

Trustworthy gold IRA companies help with the rollover process from start to finish. The better ones are transparent about fees, product eligibility, storage arrangements, and paperwork requirements.

If you need a place to start, check out our guide to the most reputable gold IRA rollover companies. Beyond that, there are a couple of basic ground rules worth keeping in mind:

1. Reputation and Prestige

A company’s reputation and customer satisfaction profile matter a great deal when shopping for a gold IRA provider. Unfortunately, some firms are more aggressive than others, especially when it comes to higher-markup products or vague fee explanations.

Avoid any precious metals company that is poorly reviewed or difficult to verify online. Customer-generated reviews on Google, Trustpilot, Reddit, the Better Business Bureau, and other platforms can help you spot recurring issues or red flags.

For a physical precious-metals IRA, IRS rules generally require that metals be held by an IRA custodian or trustee and stored through approved custody arrangements rather than personally stored at home. If a provider promotes home storage, pushes questionable coins, or refuses to confirm product eligibility in writing, that should raise concern. To stay on the safe side, review our guide to IRA-approved precious metals.

2. Rollover Limitations

Bear in mind that the IRS generally allows one indirect IRA-to-IRA rollover per 12-month period. This limit does not apply to trustee-to-trustee transfers or most direct rollovers from employer plans to IRAs. Because of this rule, many investors prefer direct transfers or direct rollovers whenever possible.

List of Top Gold IRA Companies

With so many precious metals IRA companies in the market, it can be hard to decide which one is best for your needs. That’s why comparing fee transparency, storage setup, reputation, and product selection side by side is so important before you commit.

Noble Gold

A strong all-around choice for investors who want a well-known gold IRA provider with a straightforward onboarding process, solid educational materials, and broad mainstream appeal.

GoldenCrest Metals

A solid option for investors who want more flexibility around coin and bullion choices and prefer working with a provider that emphasizes product selection.

Augusta Precious Metals

Often favored by investors who want a more consultative feel, more hand-holding during the rollover process, and a service model that tends to appeal to larger account sizes.

Generally, you should expect to pay some combination of setup fees, annual administrative fees, storage costs, insurance, and buy or sell spreads with a reputable provider. Some companies waive certain charges for the first year, but it is still smart to ask for the full fee schedule in writing before opening an account. IRS rules also require IRA metals to be held by an approved trustee or depository, which is why home storage claims should be viewed with caution.

For a more in-depth analysis of the market, read our reviews of the top 10 gold IRA providers. There you’ll find a broader breakdown of major companies in the space along with key considerations to keep in mind when comparing them.

Eligible Account Types for a Gold IRA Rollover

To complete a gold IRA rollover, you may be able to transfer funds from several types of tax-advantaged retirement accounts, including the following:

- Traditional or Roth IRA

- Self-directed 401(k)

- Employer-sponsored 401(k)

- SEP IRA

- 403(b)

- 457(b)

- TSP

In the case of employer-sponsored accounts, such as a 401(k) or 457(b), you may need to complete the rollover after terminating employment, depending on your plan’s rules. In some cases, a partial rollover may be available while you are still employed, often after reaching age 59½.

Moving funds from an existing account to a new gold IRA is usually a matter of opening a self-directed IRA through a gold IRA provider and then submitting a transfer or rollover request form. Timelines vary by custodian and plan administrator, but many rollovers and transfers are completed within roughly 1 to 3 weeks.

Gold IRA Rollover FAQs

Is a gold IRA rollover taxable?

It is usually not taxable if it is handled properly as an eligible rollover or direct transfer between retirement accounts. Problems tend to arise when an indirect rollover is mishandled or deadlines are missed.

What is the safest way to move retirement money into a gold IRA?

In many cases, the safest path is a direct rollover from a former employer plan or a trustee-to-trustee transfer between IRAs. Those methods reduce timing mistakes and withholding issues.

How long do I have to complete an indirect rollover?

You generally have 60 days from the date you receive the distribution to complete an eligible rollover. Missing that window can create a taxable event unless an exception or waiver applies.

Can I store IRA gold at home?

Generally, no. IRA-owned precious metals are typically required to remain under approved custody and storage arrangements if you want to preserve the account’s tax-advantaged status.

Can I rollover a current employer 401(k) into a gold IRA?

Sometimes, but not always. It depends on your employer plan’s rules. Some plans allow in-service rollovers or partial rollovers under certain conditions, while others do not.

What metals are usually allowed in a gold IRA?

Certain gold, silver, platinum, and palladium bullion products may qualify if they meet IRS standards and are held properly through an approved custodian or trustee. Not all coins qualify, and many collectibles do not.

What is the difference between a rollover and a transfer?

In simple terms, a transfer usually moves IRA funds directly from one custodian to another, while a rollover can involve money being distributed and then redeposited. Direct movements are generally simpler and lower risk.

Are You Ready to Start Your Rollover?

If you’re sure that a gold IRA rollover is right for you, you can get started by browsing our list of the best gold IRA companies. There you’ll find the information you need to compare providers, review fees, and better understand the rollover process.

While you’re at it, you may also want to explore other self-directed retirement options. For example, some investors choose to add a Bitcoin IRA or review whether it makes sense to hold other cryptocurrencies inside an IRA or 401(k) as part of a broader diversification strategy.

Gold: $4,341.92

Gold: $4,341.92

Silver: $63.48

Silver: $63.48

Platinum: $1,749.79

Platinum: $1,749.79

Palladium: $1,380.17

Palladium: $1,380.17

Bitcoin: $64,960.72

Bitcoin: $64,960.72

Ethereum: $1,916.46

Ethereum: $1,916.46