- GOLD IRA

- Download Our 2024 Precious Metals IRA Investor’s Guide.

Click Here

Gold IRA

Gold IRA

- Investing

-

- CRYPTO IRA

- PRICES & STATS

- RETIREMENT PLANS

Questions? Call (888) 820 1042

Questions? Call (888) 820 1042

Silver

Silver Gold

Gold Platinum

Platinum Palladium

Palladium Bitcoin

Bitcoin Ethereum

EthereumStocks, Bonds, Commodities and Currencies: The Whys and Why Nots

Disclosure: Our content does not constitute financial advice. Speak to your financial advisor. We may earn money from companies reviewed. Learn more

Last Updated on: 4th January 2016, 04:13 pm

Two recent articles sum up how challenging the past 12 months have been for many investors. In “The Year Nothing Worked: Stocks, Bonds, Cash Go Nowhere,” Bloomberg cites data from Bianco Research that shows 2015 was “the worst year for asset allocation funds since 1937,” noting that “practically every year [prior to then] has seen some asset class deliver returns exceeding 10 percent.”

Another article, “A Painful Year for Contrarian Trades,” notes the fact that a number of investments that were hit hard in 2014, and which many bargain-hunting investors had expected to rise last year, did not recover much, if at all. In fact, more than a few of the stocks and ETFs that saw double-digit percentage declines in the earlier period experienced significant drops in the subsequent span.

No one really knew that would happen, of course. No matter how much knowledge and experience we have, it is impossible to predict the future, especially in regard to markets, with any degree of certainty. Moreover, even if we are confident, for example, that U.S. interest rates will rise in 2016, as some apparently are, that doesn't necessarily mean we can forecast how asset prices will react.

A range of alternative outcomes

For one thing, it is possible that a rise in short-term yields will be viewed as negative for long-term bond prices, because of the belief that the Federal Reserve would not push rates higher unless it was confident that growth and inflation were heading higher, or that the broader interest rate framework was returning to pre-global financial crisis normality.

Then again, it is possible that market participants may see monetary policy tightening as a mistake that transforms a nascent U.S. recovery into a recession. They may also be motivated by a sense that broad deflationary forces, emanating from a slowing China or a strengthening U.S. dollar, are reason enough to own fixed-income securities, especially those with longer maturities.

Alternatively, investors and analysts may assume that the pace of rate hikes will be slower than some predict, or that the Fed may be forced to abruptly reverse course in the wake of new, more downbeat economic data, or, finally, that the Wall Street crowd will want to see multiple hikes before they are convinced that regime change is for real, before they conclude that it is time to get out of bonds.

A useful road map

The point is, as the late baseball great Yogi Berra once said, that “it's tough to make predictions, especially about the future.” However, that doesn't mean we shouldn't. It would be hard to argue that because we don't know what will happen tomorrow, or next week, or next year, we should forget about making forecasts and simply accept the risk of being blindsided or reacting unthinkingly to whatever happens.

Most would probably agree that such an approach falls short. Arguably, it is better to have some sense of what various factors, including macroeconomic, company and sector-specific fundamentals, sentiment, and technicals, suggest, and then put them in some broader probabilistic context. At the very least, this will serve as a useful road map, as well as a springboard for defining alternative approaches should things not work out as anticipated.

One place to start might be the various asset class forecasts I've posted at Gold IRA Guide. While these articles offer a personal perspective on stocks, bonds, currencies, commodities and precious metals, based on my interpretation of the available evidence, it is possible I will be wrong, or that my predictions won't come to pass until a much later date (bad timing is still wrong, by the way.)

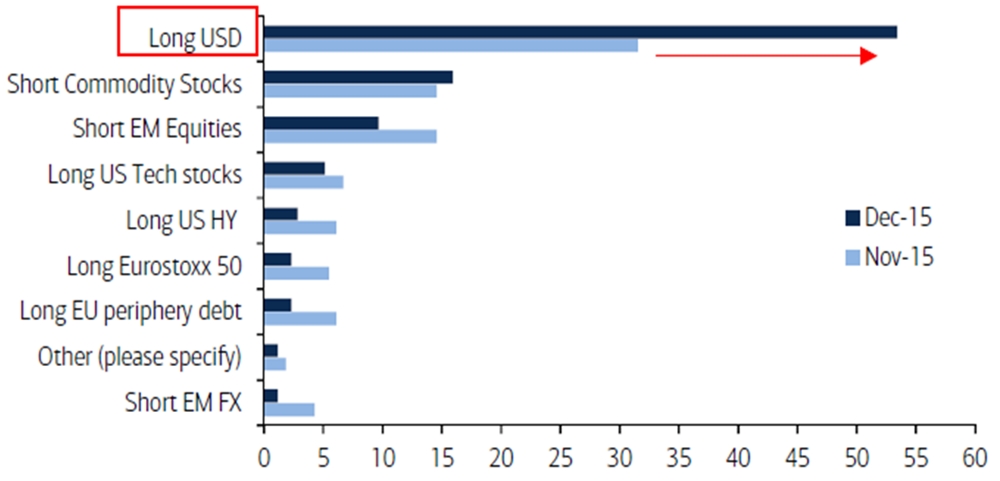

In the case of the U.S. currency, which I discussed in “U.S. Dollar: Last Currency Standing,” there are any number of things that could upend my call for a further rise. Among the most compelling, perhaps, is the fact that many participants apparently feel the same way, if the December BofA Merrill Lynch Fund Manager Survey is anything to go by. More than half of those polled believe that long U.S. dollar is “the most crowded trade.”

The key driver for this view is the expected divergence between U.S. monetary policy and that of Europe and Japan, which will, in theory at least, draw return-seeking funds away from the latter two regions and toward the former. However, with such a sizable majority betting this way, even a small change in expectations could trigger at least a short-term reversal of fortunes as nervous bulls head for the exits.

Bonds could also benefit

The prospect that monetary policy divergence might prove short-lived, perhaps because one U.S. economic data point or another turns out to be weaker than anticipated, could also boost bond prices, engendering an outcome that is at odds with what I predicted in “Anything But Positive for Bond Markets.” Even if policymakers remain silent, market participants may decide it is better to buy (bonds) first and ask questions later.

A weaker outlook for growth (or inflation), particularly if it is tied in some way to slowing Chinese economy, could also help drive raw materials prices lower, in contrast to what I forecast in “Commodities: Now’s the Time for a Contrarian Bet?” The fact that some markets fell even harder in 2015 than in 2014 makes it clear that being hated or oversold isn't necessarily the set-up for a rally. That is especially true when political elements are at play–as is the case in oil markets, where Saudi Arabia appears intent on driving out low-cost U.S. producers, which I discussed in “Awaiting the Next Crisis.”

That said, if commodity prices do, in fact, rally and inflationary expectations begin to revive, equity prices could defy an array of negatives, detailed in “The U.S. Stock Market Is Set for a Fall,” and move higher. Some market participants might even see 2015's disappointing performance as “the pause that refreshes,” or simply assume that post-2009 momentum is strong enough to power share prices higher again. There is also the possibility that low fuel prices and interest rates may finally lead consumers to open their wallets, boosting corporate revenues–as well as expectations that a bullish outlook is justified.

A better foundation

In sum, there are myriad reasons why it might be wrong to be long the dollar and commodities (including gold and other precious metals), and short bonds and equities, including some that no one, including me, has even considered. Nevertheless, by thinking about why certain outcomes make sense, and why they might not, it provides a better footing for reacting to future circumstances than the alternative.

Gold: $2,387.15

Gold: $2,387.15

Silver: $27.92

Silver: $27.92

Platinum: $931.02

Platinum: $931.02

Palladium: $903.43

Palladium: $903.43

Bitcoin: $67,910.26

Bitcoin: $67,910.26

Ethereum: $3,278.81

Ethereum: $3,278.81