Silver

Silver Gold

Gold Platinum

Platinum Palladium

Palladium Bitcoin

Bitcoin Ethereum

EthereumThe Gold/Silver Ratio: What It Is And What It Isn’t

Disclosure: We are reader-supported. If you purchase from a link on our site, we may earn a commission. Learn more

Last Updated on: 24th October 2025, 07:55 pm

Over the last couple of years, gold has set new highs and silver has climbed sharply as investors looked for safety, central banks kept buying gold, and industrial demand for silver stayed strong. If you’re deciding how to split between the two, one simple tool helps: the gold/silver ratio. This article explains what it is, why it matters, and how to use it alongside fundamentals.

Table of Contents

- What is the Gold/Silver Ratio?

- What Drives Gold in 2025

- What Drives Silver in 2025

- How Much Gold vs. Silver Should You Hold?

- Bottom Line

- Basics & Definitions

- Data & Measurement

- Macro Drivers (Gold)

- Macro Drivers (Silver)

- Strategy: Using the Ratio

- Portfolio Construction

- Instruments & Execution

- Risk Management

- Taxes & Accounts (general, not advice)

- Special Topics

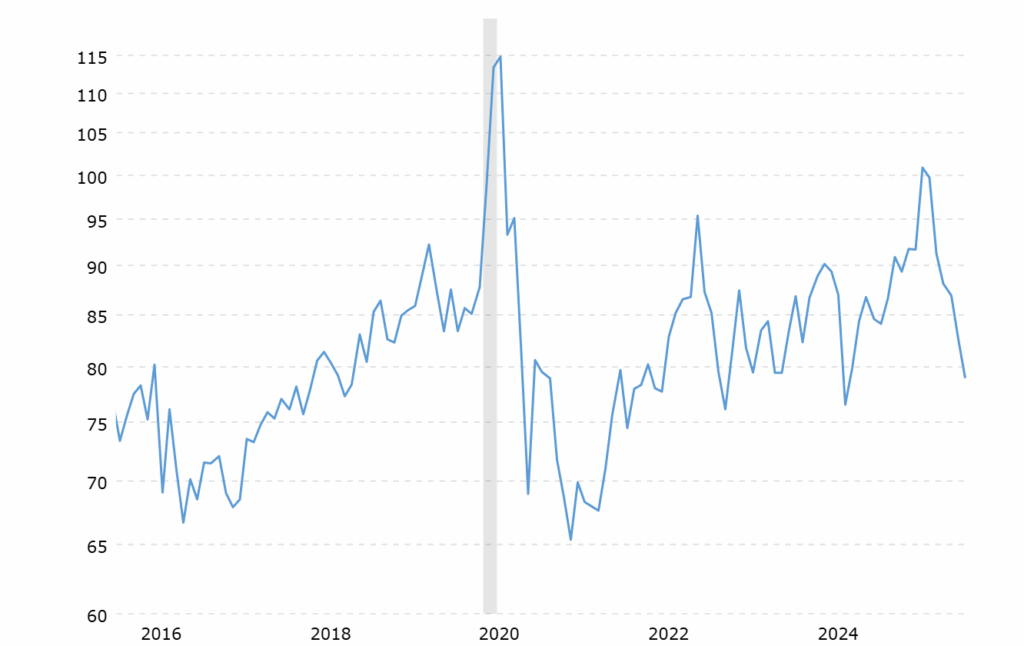

What is the Gold/Silver Ratio?

The gold/silver ratio shows how many ounces of silver it takes to buy one ounce of gold.

Formula: Gold price ÷ Silver price

Example: If gold is $2,400/oz and silver is $30/oz, the ratio is 80 (2,400 ÷ 30).

Why it’s useful: when the ratio is high, gold is expensive relative to silver (some rotate toward silver). When it’s low, gold looks cheap vs. silver (some tilt toward gold). It’s not a guarantee—use it together with fundamentals and risk controls.

Chart Sources:

- Macrotrends (Gold/Silver Ratio): https://www.macrotrends.net/1441/gold-to-silver-ratio

- TradingView

What Drives Gold in 2025

- Safe-haven & macro: Geopolitics, recession risk, and market volatility keep gold in demand when investors de-risk.

- Real rates & USD: Falling real yields and a softer U.S. dollar historically support gold.

- Central-bank buying: Many central banks continue to add to reserves, which underpins demand.

- Investment flows: Futures, ETFs, and OTC bars/coins can amplify moves during risk-on/risk-off swings.

- Jewelry & tech: Jewelry remains the largest end-use over time; electronics and other tech add a steady base.

Further reading:

World Gold Council – Gold Demand Trends: https://www.gold.org/goldhub/research/gold-demand-trends

What Drives Silver in 2025

- Industrial demand (the big one): Solar/PV, electrification, electronics, and medical uses drive most silver demand.

- Supply/demand balance: Recent years showed persistent market deficits as industrial demand outpaced mine supply and recycling.

- Investment demand: When macro risk rises, silver also benefits as a “high-beta” precious metal (it often moves more than gold—both up and down).

- Volatility: Silver typically swings more than gold; position sizing matters.

Further reading:

The Silver Institute – Supply & Demand: https://silverinstitute.org/silver-supply-demand/

How Much Gold vs. Silver Should You Hold?

There isn’t a single “right” percentage for everyone, but common ranges look like this:

- Core allocation: ~5–10% of a diversified portfolio in precious metals.

- Higher-risk periods: up to 10–15% for investors who want a stronger hedge.

How to split it:

- Balanced: 50/50 gold and silver within your metals sleeve.

- More stability: tilt to gold (e.g., 70/30) for lower volatility and better liquidity.

- More upside/volatility: tilt to silver (e.g., 30/70) if you believe industrial demand and deficits will persist.

The gold/silver ratio helps with tactical tilts: when the ratio is elevated, some add silver; when it’s compressed, some add gold. Always consider your horizon, risk tolerance, and taxes. This is educational content, not financial advice.

Bottom Line

Gold and silver still serve as useful diversifiers and potential hedges against shocks and inflation. Use the gold/silver ratio to time small tilts, but let fundamentals (rates, central-bank demand, industrial usage) drive your bigger decisions.

Want to go deeper?

- Compare gold and silver companies in 2025: Top Gold IRA company reviews

- Buying coins and bars directly? See our Top 5 silver coins for investors (add your internal link)

Gold/Silver Ratio — Advanced FAQ (2025)

Basics & Definitions

Q1) What exactly is the gold/silver ratio?

The number of ounces of silver needed to buy one ounce of gold. Formula: Ratio = Gold price ÷ Silver price.

Q2) Why do investors watch it?

It’s a relative-value gauge. When the ratio is high, gold is “rich” vs silver; when low, silver is “rich” vs gold. People use it to tilt exposure, not as a standalone buy/sell signal.

Q3) What are “normal” and “extreme” ranges?

Historically it’s floated roughly 15–100+ over long cycles. Distortions (wars, policy, liquidity shocks) can push it to extremes (e.g., >100 in crises, ~15–20 in silver manias).

Q4) Is the ratio the same worldwide?

Yes in theory, but FX moves and local premiums/taxes can shift real-world execution prices.

Data & Measurement

Q5) Which prices should I use—spot, futures, or ETF?

Use like-for-like: spot ÷ spot, front-month ÷ front-month, or ETF ÷ ETF. Mixing sources (spot gold ÷ ETF silver) introduces tracking error.

Q6) How do coin/bar premiums affect the ratio?

Compute an effective ratio with all-in costs:(Gold spot + gold premium + fees) ÷ (Silver spot + silver premium + fees).

This matters because silver’s % premiums are often higher than gold’s.

Q7) What about inflation-adjusted prices?

The ratio is already a relative measure, so CPI-adjusting both sides rarely changes conclusions for timing. It matters more when comparing across decades for macro research.

Macro Drivers (Gold)

Q8) What mainly drives gold in 2025?

- Real interest rates & USD (lower real yields, softer USD = support)

- Central-bank demand (structural buyer)

- Risk episodes (geopolitics, recession risk)

Q9) Does central-bank buying lower the ratio?

It can tilt the ratio lower if gold outperforms silver for policy reasons, but silver may still surge if industrial demand booms.

Macro Drivers (Silver)

Q10) What mainly drives silver in 2025?

- Industrial demand (solar/PV, electrification, electronics, medical)

- Supply/demand balance (recent deficit years)

- Investment flows (silver is higher beta—bigger swings than gold)

Q11) If solar demand is so strong, shouldn’t silver always outperform?

Not automatically. Mine supply, recycling, thrifting/substitution, and macro liquidity cycles can delay or mute the impact.

Strategy: Using the Ratio

Q12) How do people “trade” the ratio with physical metals?

- Rebalance bands: e.g., start 50/50; if ratio >90, shift 5–10% toward silver; if <60, rotate 5–10% toward gold.

- Threshold re-pegs: pre-define flips (e.g., at 95/80/65/50).

Document rules and review quarterly.

Q13) Can I trade the ratio with ETFs or futures?

Yes. One common method is long silver / short gold (or vice-versa) sized by dollar or volatility parity. Requires margin, roll management, and risk controls.

Q14) How long do ratio trades take to work?

They’re multi-month to multi-year mean-reversion bets. If you need near-term certainty, avoid ratio timing.

Q15) Should I wait for a “magic number” (e.g., 100) to buy silver?

No. Extremes can persist or overshoot. Scale in with staged entries rather than calling the exact top/bottom.

Portfolio Construction

Q16) How much gold vs silver should I hold?

- Core metals sleeve: ~5–10% of portfolio.

- Stress periods: up to 10–15% for stronger hedging.

Split: stability (gold) vs upside/volatility (silver). A common baseline is 60/40 gold/silver inside the sleeve.

Q17) Rebalancing cadence?

Quarterly or semiannual, or threshold-based (e.g., 20% drift from target weights). Thresholds reduce churn.

Q18) How do miners (equities) fit versus bullion?

Miners add operating leverage (and equity risk). Many investors separate a bullion allocation (defensive) from a miner sleeve (offense).

Instruments & Execution

Q19) Physical vs ETFs vs futures—pros/cons?

- Physical: no counterparty risk, but storage/insurance and higher premiums.

- ETFs/closed-end trusts: liquid, low storage burden, but management fees and potential tracking differences.

- Futures: efficient for hedging and ratio trades; needs expertise, margin discipline.

Q20) What storage choices matter for physical?

Decide on home safe vs insured vault, bar sizes (1 oz vs kilo), and liquidity (common coins/bars move faster at tighter spreads).

Q21) How do premiums behave in stress?

Spreads usually widen, especially for silver coins. Plan purchases ahead; don’t rely on last-minute fills during panics.

Risk Management

Q22) Biggest mistakes with the ratio?

- Treating it as a standalone signal

- Ignoring all-in costs and taxes

- Using too much leverage

- Not having clear exit/rebalance rules

Q23) What if the ratio stays extreme for years?

Use position sizing and time diversification. Extreme regimes can last; avoid binary all-in/all-out bets.

Q24) How does USD strength affect the ratio?

USD strength can pressure both metals, but not equally. If gold holds up better than silver, the ratio rises; the reverse can lower it.

Taxes & Accounts (general, not advice)

Q25) Any tax nuances?

- Physical bullion: usually capital gains when sold; your local rules apply.

- ETFs/trusts: distributions and gains vary by structure and jurisdiction.

- Consider tax-advantaged accounts (e.g., registered or retirement accounts such as Roth, 401k, or Traditional IRA) if eligible. Consult a professional.

Special Topics

Q26) Does platinum/palladium matter for the ratio?

Not directly, but PGM cycles can divert investor attention and capital within the metals complex, influencing relative performance.

Q27) Can above-ground stockpiles cap silver rallies?

They can buffer supply in the short run, but access, form (industrial vs investment bars), and investor hoarding behavior are variables.

Q28) Is there seasonality?

Some calendar patterns exist (wedding seasons, year-end flows), but they’re weak and inconsistent compared to macro drivers.

Q29) How do lease rates or GOFO-type dynamics matter?

Tight physical conditions can show up in lease/forward rates and may foreshadow dislocations—but interpreting them requires pro-level context.

Q30) What’s a simple, rules-based tilt I can implement today?

Example starter playbook:

- Define target split (e.g., 60/40 gold/silver).

- Band rebalancing: If ratio >90, move 5% of metals sleeve from gold→silver. If <60, move 5% from silver→gold.

- Review quarterly; cap each move to avoid over-rotation.

Gold: $4,114.78

Gold: $4,114.78

Silver: $59.24

Silver: $59.24

Platinum: $1,660.82

Platinum: $1,660.82

Palladium: $1,303.22

Palladium: $1,303.22

Bitcoin: $65,959.36

Bitcoin: $65,959.36

Ethereum: $1,919.97

Ethereum: $1,919.97