Silver

Silver Gold

Gold Platinum

Platinum Palladium

Palladium Bitcoin

Bitcoin Ethereum

EthereumHow to Become an Investor: A Guide for Beginners (2026)

Disclosure: We are reader-supported. If you purchase from a link on our site, we may earn a commission. Learn more

Last Updated on: 19th December 2025, 02:38 am

Let’s face it, not everyone has what it takes to be the next Warren Buffett or Bill Ackman. For every millionaire that financial investing produces, there are thousands who will never outperform the S&P 500.

Free 2026 Gold Investment Kit (Top-Ranked Company)

If you’re exploring gold as part of a diversified plan, Noble Gold’s free 2026 kit breaks down the basics, common mistakes, fees to watch, and how precious metals IRAs work.

Get the Free KitDisclosure: If you request the kit through our link, we may earn a commission at no extra cost to you.

In fact, many active fund managers fall short of their benchmarks over time. If full-time financial professionals can struggle to beat the market consistently, you should first ask yourself what comparative advantage you might have that can set you apart from them.

Important: This guide is for educational purposes only and is not financial, tax, or legal advice. If you’re unsure what’s appropriate for your situation, consider speaking with a licensed professional.

Nonetheless, countless investors do succeed in the markets every day. For those who want to play their hand, it’s important that you do your homework and your due diligence in order to understand the risks you will face and manage them appropriately.

Table of Contents

Entering the world of financial markets can be both exhilarating and overwhelming, especially for beginners. The allure of potentially substantial gains and the opportunity to build wealth can be enticing, but it's essential to approach the financial markets with caution and a solid understanding of the risks involved.

Understanding the Basics

Before diving into the intricate world of financial markets, it's crucial to understand the foundational concepts:

- Types of Financial Markets:

There are several types of financial markets, including the stock market (equity market), bond market, foreign exchange market (forex), and commodities market. Each has its unique characteristics and involves trading different types of assets.

- Investment Vehicles:

Common investment vehicles include stocks, bonds, mutual funds, exchange-traded funds (ETFs), and options. These instruments allow investors to participate in various markets with different levels of risk and potential return.

- Risk and Reward:

The financial markets offer opportunities for both profit and loss. Generally, higher potential returns come with higher risks. Understanding your risk tolerance is crucial in designing your investment strategy.

Steps for Beginners

- Education:

Begin by educating yourself. Read books, take online courses, and follow reputable financial news sources. Understanding market dynamics, investment strategies, and economic indicators will empower you to make informed decisions.

- Set Clear Goals:

Determine your financial goals. Are you investing for retirement, buying a house, or simply looking to grow your wealth? Your goals will guide your investment approach. If retirement is your main objective, it helps to understand the main types of retirement plans first.

- Create a Budget:

Assess your financial situation and establish a budget for investing. Never invest money you can't afford to lose. Also, consider tackling high-interest debt first so your money is not working against you.

- Start Small:

Begin with a small amount of money. This allows you to gain experience without risking significant losses. As you become more confident, you can gradually increase your investment.

- Diversification:

Spread your investments across different asset classes to reduce risk. Diversification helps mitigate losses if one investment performs poorly. If you’re adding precious metals, you may also want to understand silver vs. gold and how each tends to behave across market cycles.

- Long-Term Perspective:

Keep a long-term perspective. Trying to time the market or chasing short-term gains can lead to poor decisions and losses. Patience is a key virtue in investing.

- Seek Professional Advice:

Consider consulting with a financial advisor. Their expertise can help tailor an investment strategy that aligns with your goals and risk tolerance.

Navigating the Risks

While the potential for gain in the financial markets is appealing, it's vital to be aware of the associated risks:

- Market Volatility:

Prices of assets can fluctuate dramatically due to various factors like economic news, geopolitical events, and market sentiment. This volatility can lead to sudden losses.

- Lack of Control:

Investors have limited control over external events that can impact their investments. Regulatory changes, unexpected company developments, or global crises can disrupt markets.

- Leverage:

Some markets allow the use of leverage, which magnifies gains but also amplifies losses. Novice investors may find themselves in a precarious position if they don't fully understand how leverage works. If you use margin, learn how margin calls work before you place your first leveraged trade. A practical overview: FINRA’s margin basics.

- Emotional Decision-Making:

Emotional reactions to market movements can lead to impulsive decisions. Fear and greed are powerful emotions that can cloud rational judgment. If you want a deeper dive on this exact problem, see: emotional investing tips.

- Scams and Fraud:

Financial markets can attract unscrupulous individuals looking to exploit inexperienced investors. Be cautious of get-rich-quick schemes and always do thorough research. If you want a quick checklist of common red flags, see our guide on investment and gold scams. You can also review the U.S. regulator’s general guidance on spotting fraud: SEC Investor Alerts.

Picking a Winning Investing Strategy

Learning how to become an investor starts with choosing an investing strategy that works with your expected time horizon and risk tolerance. Below, we’ve outlined a few common investing strategies that are often employed by certain age cohorts depending on their appetite for risk.

Conservative Portfolio for Retirees (Low Risk Tolerance)

- Age: 65+

- Risk Tolerance: Low

- Strategy: Capital preservation and income generation.

- Example Portfolio Allocation:

- – 50% Bonds (Government and Corporate)

- – 30% Cash and Equivalents

- – 10-15% Real Estate Investment Trusts (REITs)

- – 5-10% Precious Metals (Gold and Silver)

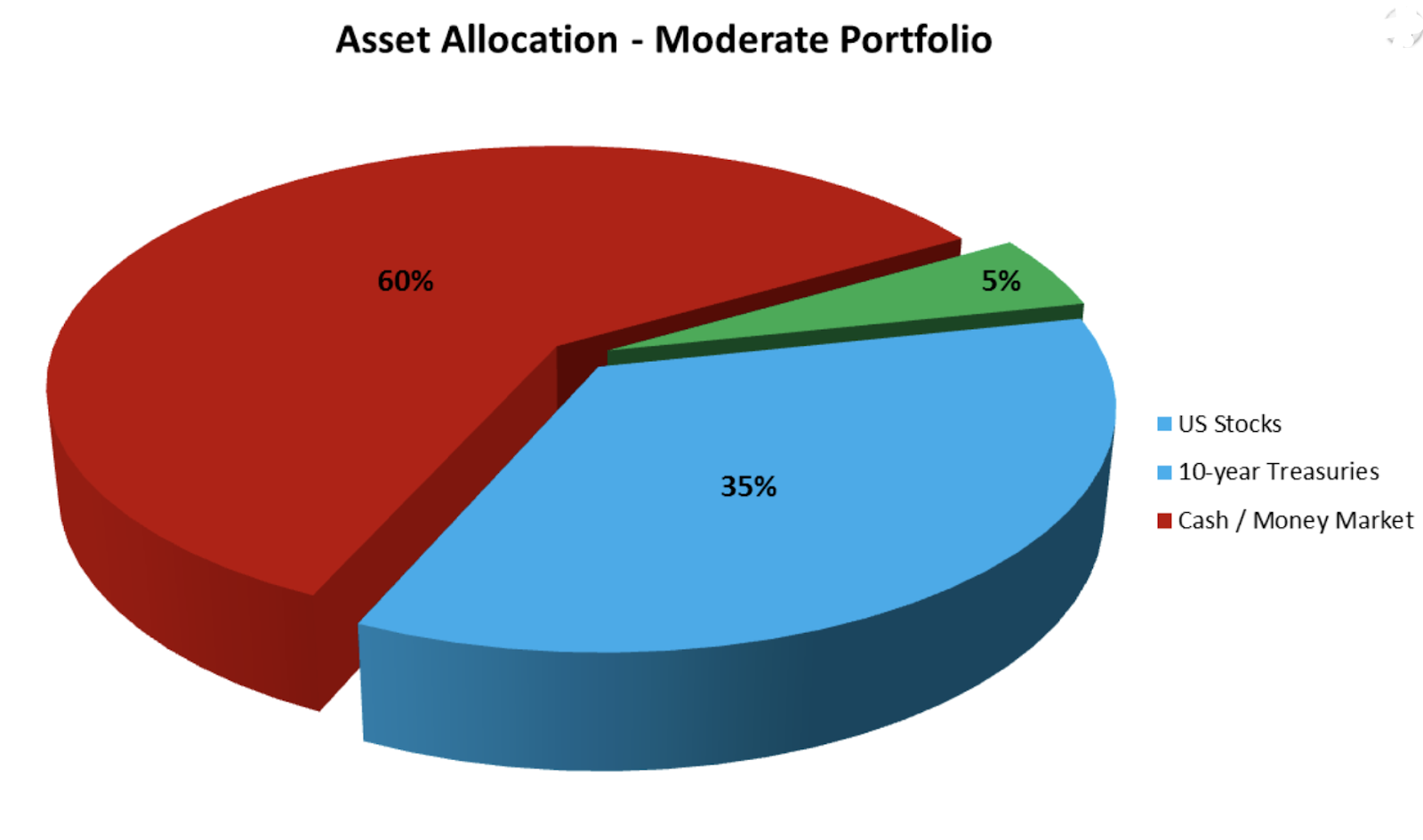

Balanced Portfolio for Middle-Aged Investors (Moderate Risk Tolerance)

- Age: 40-55

- Risk Tolerance: Moderate

- Strategy: Balanced growth and income.

- Example Portfolio Allocation:

- – 50% Stocks (Diversified)

- – 30% Bonds (Government and Corporate)

- – 5-10% Cash and Equivalents

- – 5-10% Real Estate & Precious Metals (Gold and Silver)

Growth Portfolio for Young Professionals (Moderate to High Risk Tolerance)

- Age: 25-35

- Risk Tolerance: Moderate to High

- Strategy: Capital growth with a long-term focus.

- Example Portfolio Allocation:

- – 70% Stocks (Diversified, including international)

- – 15% Bonds (Short-term and High-Yield)

- – 10% Cash and Equivalents

- – 5% Alternative Investments (Cryptocurrencies or Precious Metals)

Aggressive Growth Portfolio for Young Investors (High Risk Tolerance)

- Age: 18-30

- Risk Tolerance: High

- Strategy: Aggressive capital growth.

- Example Portfolio Allocation:

- – 80% Stocks (Mainly Growth and Tech)

- – 10% Alternative Investments (Cryptocurrencies or Precious Metals)

- – 5% Bonds (Short-term for stability)

- – 5% Cash (Opportunistic)

Income-Oriented Portfolio for Pre-Retirees (Moderate Risk Tolerance)

- Age: 55-65

- Risk Tolerance: Moderate

- Strategy: Income generation for retirement.

- Example Portfolio Allocation:

- – 40% Bonds (Government, Corporate, Municipal)

- – 30% Dividend-Paying Stocks

- – 20% Real Estate (REITs or Direct Investments)

- – 10% Cash and Equivalents

Sustainable Investment Portfolio for Ethical Investors (Moderate Risk Tolerance)

- Age: Any

- Risk Tolerance: Moderate

- Strategy: Investing with a focus on environmental, social, and governance (ESG) principles

- Example Portfolio Allocation:

- – 50% ESG-Compliant Stocks (Sustainable companies)

- – 30% Green Bonds (Funding eco-friendly projects)

- – 10% Real Assets (Renewable energy, sustainable agriculture)

- – 10% Cash (Opportunistic)

The “Recession Proof” Portfolio for Risk Management

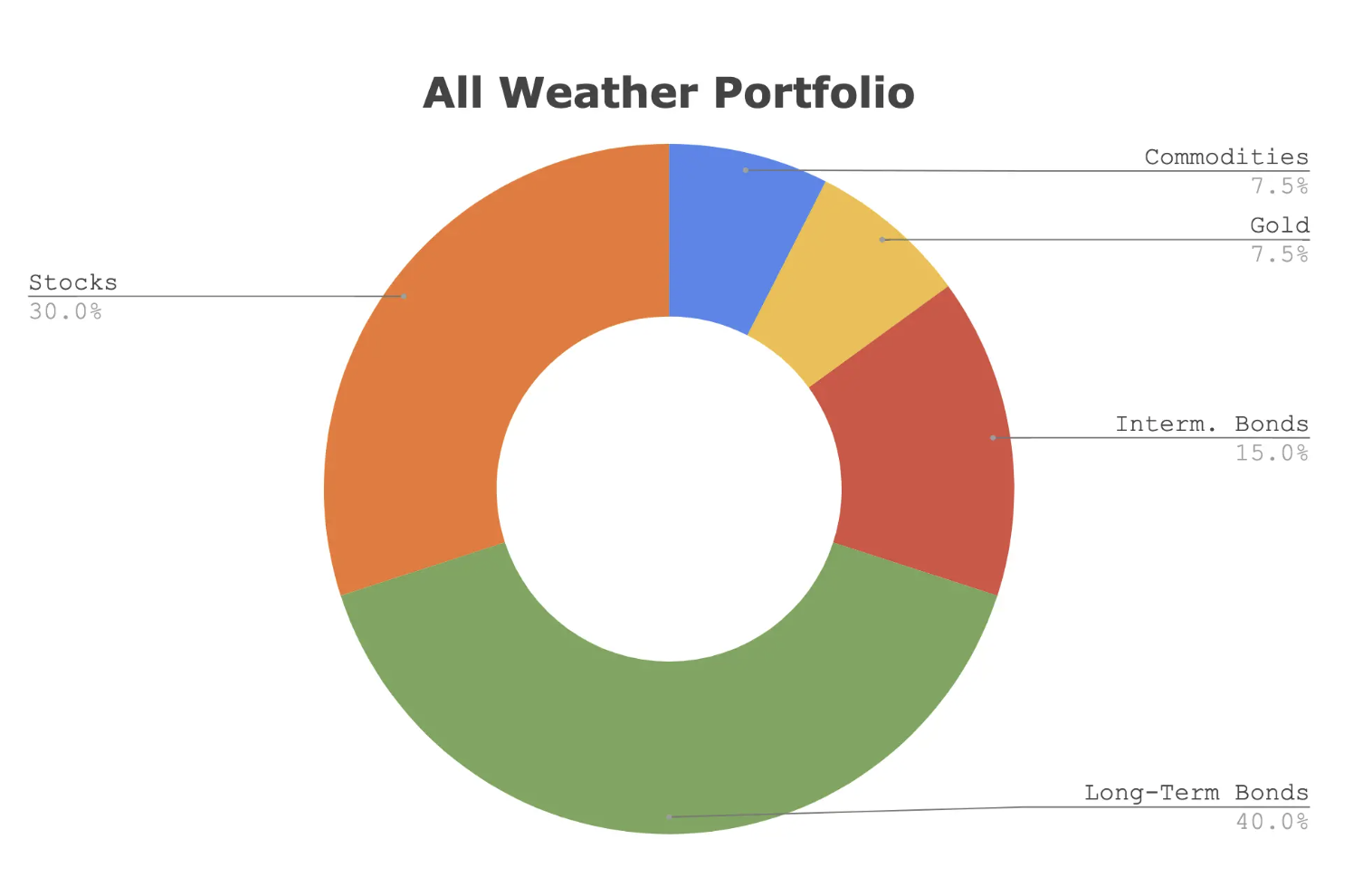

Perhaps the best-known investment portfolio for managing risk is investor Ray Dalio’s “All Weather” portfolio. His is a medium-risk strategy designed to survive recessions while capturing significant upside potential in bull markets.

Historically, the All Weather portfolio has averaged a 7.17% annual compound return over the past 30 years, which is only slightly shy of the performance of the S&P 500 Index.

Ray Dalio’s signature recession-resistant portfolio (Source: OptimizedPortfolio)

However, Ray Dalio’s portfolio bears greater risks than some investors would care to be exposed to. For instance, a 30% allocation to stocks can inject a lot of volatility into one’s portfolio, especially during periods of systemic instability.

To hedge against broad market risks such as recessions and long-term bear markets, some investors may opt for a “recession-proof” portfolio. While no investment is truly free from the risks of recessions, this investing strategy provides perhaps the greatest degree of shelter from recessionary activity out of any model portfolio. If you want to understand the moving parts behind downturns, start here: what happens in a recession.

Originally popularized by ChatGPT, the recession-proof portfolio suggests the following asset allocation that is naturally well-suited for risk-averse investors:

- Bonds: 40%

- Defensive Stocks: 30%

- Gold and Precious Metals: 20%

- Cash: 10%

The absence of high-upside assets, such as cryptocurrencies, real estate, and growth stocks, and the heavy weighting of cash, precious metals, and bonds, make this portfolio more “defensive” in nature in order to protect against volatility and asset depreciation.

Remember, these are general guidelines, and individual circumstances will vary. It's important for investors to regularly review and adjust their portfolios based on changing financial goals, market conditions, and risk tolerance.

It’s always best to consider seeking advice from a financial advisor to create a personalized investment strategy that aligns with your specific needs and objectives.

Choosing an Investment Company to Get Started With

If you want to become an investor, you need to carefully select the firm with which you open an account. For many, a simple brokerage account will do the trick.

In fact, 17 million Americans own an investment account with big-name brokerages such as Vanguard, Charles Schwab, and Fidelity Investments.

Be warned, though, that costs can add up depending on what you use. The brokerage account itself may be low-cost, but advisory management (if you hire an advisor), fund expense ratios, trading costs, and platform services can all affect your returns. For a simple overview of how fees can impact long-term growth, see Investor.gov’s explanation of fees and expenses.

Aside from the fees and commissions, brokerages also usually dictate which assets you can and cannot invest in. Investors who want full financial freedom may want to explore alternative solutions in order to invest in assets typically unpermitted by brokerages, such as real estate, Bitcoin, and gold or silver.

Self-directed individual retirement accounts (SDIRAs) are alternative investment vehicles that are not offered by brokerages. Instead, dedicated third-party companies offer these account types to allow independent investors to invest in the kinds of assets they want, with fewer rules, no active management, and far greater financial freedom. If you’re comparing retirement accounts, you might also like our breakdown of 403(b) vs. 401(k).

While these account types aren’t for everyone, they can provide the tools needed to accelerate one’s investing progress and achieve their goals faster than they otherwise would. This is because SDIRAs allow for greater asset class diversification and risk management.

Thinking about a Gold IRA? Grab the free 2026 kit and skim the “fees and mistakes” sections before you commit to anything.

Request the Free 2026 KitDisclosure: We may earn a commission if you request the kit through our link.

Our 3 Top-Ranked SDIRA Companies

Below, we’ve listed our three top-rated SDIRA companies to help you kickstart your alternative investing journey. Although these companies specialize in precious metals assets, their SDIRA accounts allow for any combination of conventional and alternative asset holdings.

Noble Gold boasts some of the most competitive fees in the bullion industry, along with exemplary ratings compared to all the companies we assessed in 2024.

Co-founders Charles Thorngren and Collin Plume opted not to allocate millions of dollars to hire celebrity ambassadors or produce extravagant television and radio commercials. Instead, they chose to operate a streamlined business, prioritizing exceptional client service.

This strategy appears to be yielding positive results, with the company consistently receiving outstanding ratings. We encountered only a single 2020 complaint on the Better Business Bureau (BBB), which has since been resolved.

(Want to learn more about Noble Gold? Read our full Noble Gold review here.)

Quick Notes:

- Lowest fees in the industry

- Low account minimums ($2,000)

- No-hassle buyback policy for all gold and silver

- IRS-approved storage facilities in Texas

- Relatively new company (founded 2017)

What an impressive track record! It's no wonder we've selected Augusta Precious Metals as one of our top recommended gold IRA companies.

Among the 70+ companies we reviewed, Augusta Precious Metals stood out with its exceptional ratings and reviews on platforms such as the Better Business Bureau (BBB), Business Consumer Alliance (BCA), Google, and more. Money magazine even honored this company with the title of “Best Overall” Gold IRA Company.

Augusta Precious Metals has gone the extra mile by adding a Harvard-trained economic analyst, Devlyn Steele, to their team, offering valuable education to potential customers considering precious metals investments. One can also take inspiration from the endorsement of Hall of Fame quarterback Joe Montana, who entrusted Augusta Precious Metals to be his gold company of choice. He's not only a customer but also a passionate advocate.

If you decide to partner with Augusta Precious Metals, rest assured, you won't be disappointed.

(Interested in Augusta Precious Metals? Read our full Augusta Precious Metals review here.)

Quick Notes:

- Best ratings across the board

- Zero fees for up to 10 years for all customers

- Money Magazine’s “Best Overall” Gold IRA company

- Relatively high account minimum ($50,000)

- Endorsed by Hall of Fame quarterback Joe Montana

Silver Gold Bull is a reputable precious metals investment firm with offices in Las Vegas, Nevada, and Calgary, Alberta. This Canadian-American company boasts an extensive inventory of precious metals products, characterized by remarkably low markups, averaging just 3%.

Their diverse range of bullion options caters to the preferences of retirement savers, investors, and collectors alike. For American customers, Silver Gold Bull collaborates with a range of IRA providers, simplifying the process of rolling over IRAs or 401(k)s into precious metals.

Similarly, for Canadian clients, the company offers a seamless avenue for diversifying Registered Retirement Savings Plans (RRSPs) and other Canadian registered savings plans into physical precious metals bullion. In addition to their highly competitive markups, Silver Gold Bull ensures complete product insurance and refrains from charging any startup fees. If you’re new to precious metals, you may also like our beginner guide on how to buy silver and gold.

(Thinking of opening an account with Silver Gold Bull? Check out our full Silver Gold Bull review first.)

Quick Notes:

- U.S. and Canadian storefront shopping experience available

- “Best Price Guarantee” on gold bars

- Terrific selection of RRSP, TFSA, and IRA-eligible products

- Limited selection of platinum and palladium products

- Low markups of only about 3% on average

Become an Investor: Open an SDIRA Today

Knowing how to become an investor starts with knowing how to open an account. While a brokerage account may be beneficial for hands-off investors, more active investors will likely prefer to open an SDIRA, a tax-advantaged retirement account that allows for any and all assets to be held within it.

Note that venturing into the financial markets as a beginner can be a rewarding journey if approached with the right knowledge, mindset, and caution. Remember that while the potential for financial gain is real, so are the risks. Educate yourself, set clear goals, and develop a well-thought-out strategy that aligns with your risk tolerance.

Be vigilant, stay informed, and be prepared to adapt to changing market conditions. By treading carefully and making informed decisions, you can navigate the complexities of the financial markets and work towards achieving your financial aspirations.

FAQ (Quick Answers for New Investors)

How much money do I need to start investing?

Often, you can start with a small amount. The more important question is whether you have (1) an emergency fund, (2) manageable high-interest debt, and (3) a plan to invest consistently. Starting small and building the habit is usually better than waiting for the “perfect” amount.

Should I buy individual stocks or start with ETFs and index funds?

Many beginners start with diversified ETFs or index funds because you instantly spread risk across many companies. Individual stocks can work, but they require more research, more discipline, and often come with bigger portfolio swings.

What account should I open first: 401(k), IRA, Roth IRA, or brokerage?

It depends on your situation, but many people prioritize employer retirement plans (especially if there’s a match), then compare IRA vs Roth IRA options, and then use a taxable brokerage for additional investing. If you’re investing for retirement, start by understanding the account rules and contribution limits for the plan(s) you have access to.

How do I know my risk tolerance?

A simple test is this: if your portfolio dropped 20% in a bad year, would you panic-sell or stick to your plan? Risk tolerance is part math (time horizon, income stability, emergency fund) and part psychology (how you handle volatility). If you lose sleep over swings, you likely need a more conservative allocation.

How often should I check my portfolio?

For long-term investors, checking too often can fuel emotional decisions. Many people review monthly or quarterly, and rebalance once or twice per year, or when allocations drift materially from targets.

What is dollar-cost averaging and does it work?

Dollar-cost averaging means investing a fixed amount on a schedule (weekly, biweekly, monthly). It can reduce the stress of “timing the market” and helps you stay consistent through ups and downs. It does not guarantee profits, but it often helps beginners stay disciplined.

How do I avoid scams and shady “gurus”?

Be skeptical of guaranteed returns, urgency tactics, secret strategies, and anything that discourages independent verification. Confirm licensing where relevant, read third-party reviews, and compare claims against regulator guidance. If something sounds too good to be true, it usually is.

Where do gold and precious metals fit for a beginner?

Many portfolios use precious metals as a diversifier or hedge, often as a smaller allocation. The “right” percentage depends on your goals, your time horizon, and how much volatility you can handle. If you’re considering a Gold IRA or physical metals for retirement, make sure you understand fees, storage, liquidity, and buyback policies first.

Is a self-directed IRA a good idea for everyone?

Not necessarily. SDIRAs can unlock more asset choices, but they also add complexity and responsibility. They tend to be a better fit for investors who want alternative assets and are willing to do the extra due diligence, including understanding custodians, storage (for metals), and fee schedules.

Gold: $4,048.80

Gold: $4,048.80

Silver: $57.37

Silver: $57.37

Platinum: $1,613.93

Platinum: $1,613.93

Palladium: $1,275.60

Palladium: $1,275.60

Bitcoin: $63,707.59

Bitcoin: $63,707.59

Ethereum: $1,887.71

Ethereum: $1,887.71