Silver

Silver Gold

Gold Platinum

Platinum Palladium

Palladium Bitcoin

Bitcoin Ethereum

EthereumRisk-Free Rate: Theoretical Myth or Financial Reality?

Disclosure: We are reader-supported. If you purchase from a link on our site, we may earn a commission. Learn more

Last Updated on: 23rd August 2023, 07:19 pm

In finance, where uncertainty reigns supreme, one concept stands out as both fundamental and elusive: the risk-free rate. This metric serves as a cornerstone for a multitude of financial calculations, yet its existence as a “real” benchmark or a mere theoretical construct remains a subject of debate.

The so-called “risk-free rate” is a conceptual tool used for pricing financial products. It refers, in short, to the interest rate on an investment with absolutely no risk of not being paid back. It’s a starting point in determining the potential return on a given investment that carries no risk.

However, all investments carry some type of risk. Even triple-A government bonds, as we’re about to discover, are exposed to various types of market risk.

A truly risk-free investment would generate no return, nullifying its use as an investment. Even sovereign states and financial institutions cannot agree on standardized risk-free rates—rather, they change depending on the jurisdiction and its macroeconomic conditions.

Therefore, the concept of a “risk-free rate” is indeed fluid and only exists as a tool for lenders and creditors to estimate rates of return on riskier investments.

Now, let’s get into the nitty-gritty and fully define a risk-free rate, explore its significance and practical implications, and discuss how to calculate a risk-free rate.

Table of Contents

Understanding the Risk-Free Rate

When you hear about the risk-free rate, it's usually used as a benchmark for comparing the potential returns of other investments.

Let's say you're thinking about investing in a stock or a business venture. You would compare the potential return of that investment to the risk-free rate to determine if it's worth taking on the additional risk.

Remember, while the concept of a risk-free rate is essential in finance, there is no investment that is entirely without risk. Different investments offer different levels of risk, and the risk-free rate helps you gauge whether an investment is worth the risk you're taking.

To reiterate, the risk-free rate is like the foundation of a building. It's the minimum return you'd expect from an investment that involves zero risk, and it helps you assess whether other investments are worth the risk they come with.

Discovering the Risk-Free Rate

Governments issue bonds, which are essentially promises to repay borrowed money with interest over a specified period.

The yield or interest rate on these bonds is typically used as a proxy for the risk-free rate because governments are considered very unlikely to default on their debt obligations.

(By the way, this brief article comparing gold to “paper gold” helps explain how default risk and counterparty risks affect virtually all asset types.)

This is especially true for countries with “AAA” credit ratings from agencies like S&P Global Ratings, Fitch, and Moody’s. At present, countries such as Luxembourg, Switzerland, Singapore, and the Netherlands all have triple-A credit ratings.

At the time of writing, a Swiss 10-year treasury bond carries a 0.953% yield as of August 2023.

Therefore, one could consider 0.953% to be a “risk-free rate of return” on their investment since the Swiss government has a perfect track record of meeting its debt obligations.

Unraveling the Risk-Free Rate

At its essence, the risk-free rate is the theoretical interest rate that an investor can expect to earn on an investment that carries no risk whatsoever.

In the realm of finance, risk and return are intrinsically linked. Investors generally demand a higher return for bearing greater risks.

Hence, the risk-free rate serves as a reference point against which the expected returns of other investments are measured.

In most cases, this rate is often associated with the yield on a government-issued bond, commonly from a stable and economically robust country like the United States or, in the example above, Switzerland.

Note that the United States was downgraded to a second-tier “AA+” rating from both Fitch and S&P in early August 2023. Their triple-A rating remains intact with Moody’s.

The Real vs. Theoretical Dilemma

One of the central quandaries surrounding the risk-free rate is, well, its actual existence. Critics argue that in a world where all investments inherently carry some degree of risk, the notion of a completely risk-free asset is little more than a theoretical abstraction.

Even sovereign bonds, typically perceived as risk-free, are exposed to uncertainties like inflation and interest rate fluctuations. Furthermore, the concept assumes perfect market conditions and assumes a world without credit risk, liquidity risk, or even the potential for government default.

In the case of the Swiss example provided above, inflation risk still presents a real threat. As of Q2 2023, the Swiss inflation rate is 1.7%—a figure exceeding their 10-year treasury yield by over 75%.

In other words, not even the Swiss treasury yield can be considered “risk-free” because the Swiss franc is still subject to depreciation in purchasing power over time.

Practical Applications and Interpretations

While skeptics question its tangibility, the risk-free rate is undeniably pervasive in the finance landscape. It's the foundation for calculating the cost of capital, which helps businesses evaluate potential investments.

The Capital Asset Pricing Model (CAPM), a widely used tool in modern finance, incorporates the risk-free rate to estimate the appropriate expected return on an asset given its risk relative to the market. This model, though criticized for its assumptions, forms the basis for many investment decisions on Wall Street and beyond.

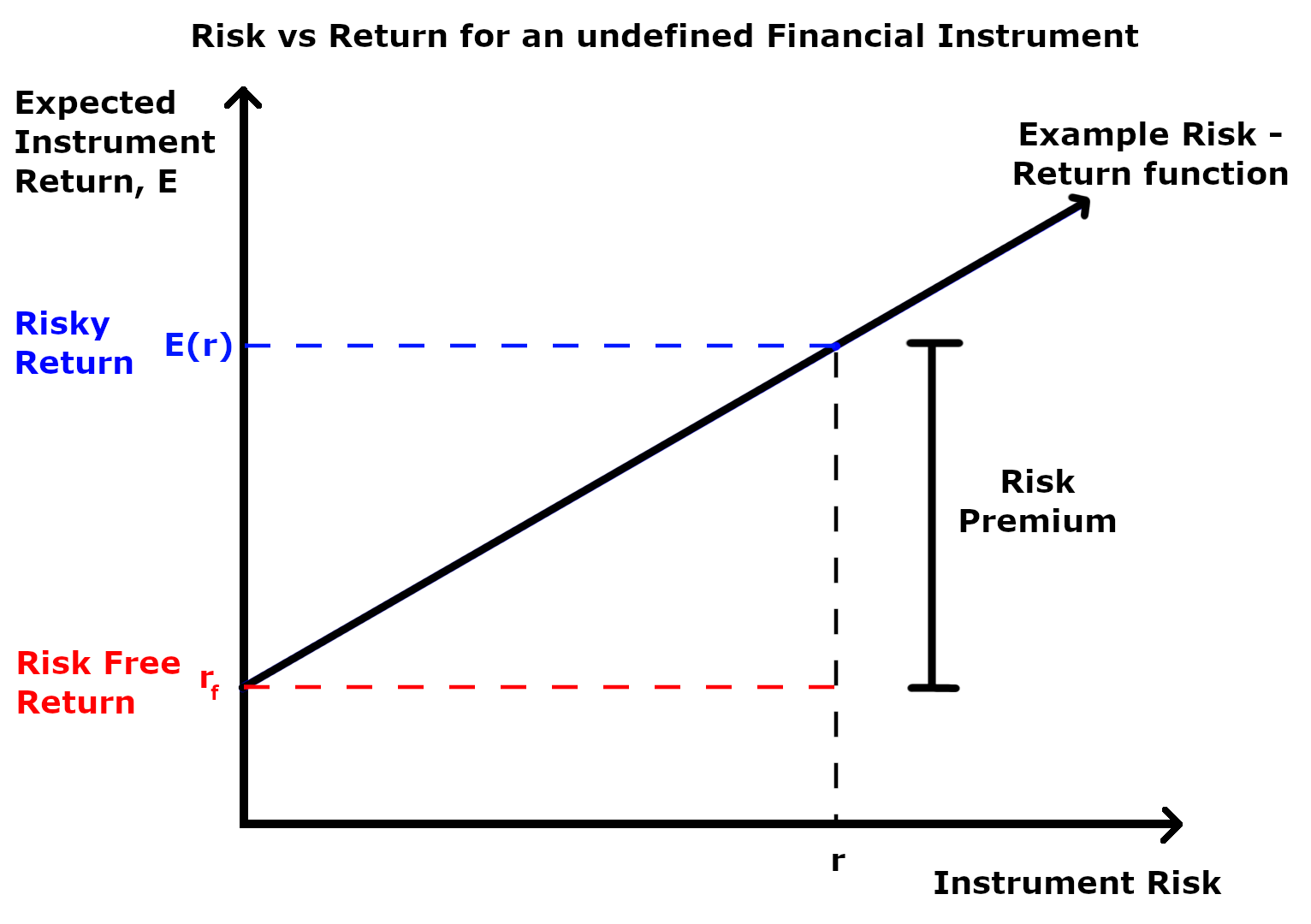

In financial markets, investors and creditors price assets (or establish the “cost of equity”) by taking the current risk-free rate and adding the beta and equity risk premium.

Source: Wikimedia Foundation

Because individual securities are more volatile than large indices, and the market as a whole, this is numerically represented as “beta” and added to the risk-free rate of return. The chart above depicts the risk premium captured by CAPM pricing model.

Market Realities and Divergence

Critics of the risk-free rate's existence often point to the disparity between theoretical predictions and real-world market conditions. In practice, the risk-free rate can vary greatly based on factors like macroeconomic trends, investor sentiment, and central bank policies.

This volatility highlights the challenges of relying on a singular benchmark for valuation and investment decision-making.

In any case, the risk-free rate should be considered an imperfect tool for calculating asset prices and risks. Nonetheless, it is used widely by investment bankers and investors via the CAPM asset pricing model to assign values to entities of otherwise unknown value.

So while the risk-free rate may not be as “risk-free” as its name suggests, its presence as a theoretical tool cannot be disregarded. In a world where market participants require a baseline for assessing risk and return, the risk-free rate provides a valuable starting point.

Despite this, it is crucial to acknowledge its limitations and the potential divergence between theory and reality.

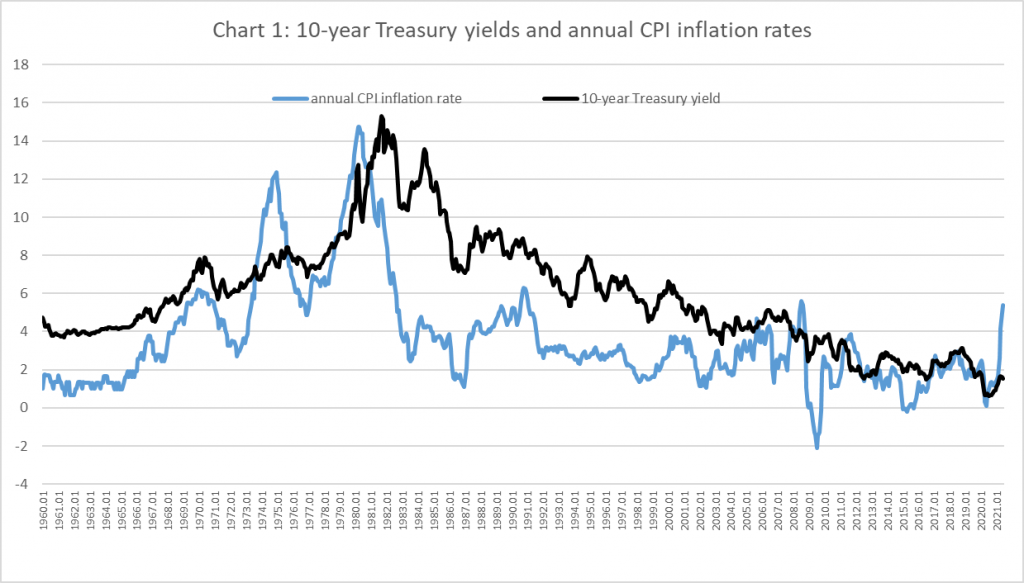

Source: American Enterprise Institute

The chart above aptly demonstrates the risks inherent to even the “safest” investment classes. In this case, 10-year Treasury yields are outmatched by the consumer price index (CPI) at multiple points in recent history—including the recent inversion that began in 2021.

The Bottom Line: Myth or Reality?

The risk-free rate represents a unique amalgamation of theory and practice in finance. While it may not truly exist in its idealized form, its role in financial models and valuations is undeniable.

In sum, the risk-free rate is both a theoretical tool and a practical necessity in the world of finance. Its presence as a benchmark guides investment decisions and valuation models, even as its “risk-free” nature is continually challenged by the inherent uncertainties of the market.

As investors and analysts continue to grapple with the complexities of risk and return, the risk-free rate stands as a constant reminder of the delicate balance between theoretical constructs and the pragmatic intricacies of the market.

Investors interested in managing risk in their own portfolios are encouraged to do so with a self-directed IRA—the only retirement account type that allows you full financial freedom to diversify your holdings across a wide variety of asset classes. To get started, check out this updated review of the best self-directed gold IRA companies in the Salt Lake Tribune.

Gold: $4,345.36

Gold: $4,345.36

Silver: $63.62

Silver: $63.62

Platinum: $1,758.00

Platinum: $1,758.00

Palladium: $1,383.95

Palladium: $1,383.95

Bitcoin: $64,878.05

Bitcoin: $64,878.05

Ethereum: $1,913.70

Ethereum: $1,913.70

{kind=link}