- GOLD IRA

- Download Our 2024 Precious Metals IRA Investor’s Guide.

Click Here

Gold IRA

Gold IRA

- Investing

-

- CRYPTO IRA

- PRICES & STATS

- RETIREMENT PLANS

Questions? Call (888) 820 1042

Questions? Call (888) 820 1042

Silver

Silver Gold

Gold Platinum

Platinum Palladium

Palladium Bitcoin

Bitcoin Ethereum

EthereumPeerform Review

Disclosure: Our content does not constitute financial advice. Speak to your financial advisor. We may earn money from companies reviewed. Learn more

Last Updated on: 25th March 2023, 12:10 am

Peerform

- Phone : 1-800-388-8049

- URL :

- Global Rating

- Good

User Rating

- 0 No reviews yet!

Review Summary :

Peerform has found a desperately needed niche in the under-served, 600 credit score borrower market and has built a successful Peer to Peer Lending business model on this group. Thanks to their cutting-edged proprietary algorithm, they are able to accurately price risk and return factors in the P2P lending equation. Their investor interest rate returns are better than those of their main rivals in the space, making this a very attractive platform for investors who want to diversify their holdings into a personal and small business loan portfolio.

Pros:

- If your request is approved at a lower amount than you wanted, you can choose to take the lower loan amount rather than get nothing.

- For those with less than perfect credit, this platform considers credit scores as low at 600.

- Gives out lower APR interest rates than many of its P2P space competitors do.

- Investors can take comfort in their Peerform Loan Analyzer that accurately determines the risk levels and sets returns accordingly.

Cons:

- Loan disbursement can require as long as 14 days for the loan to be funded and paid.

Quick Facts about Peerform

Reviewed By:David Crowder

Have you purchased products from Peerform? Leave a review!

Eventually you had to figure some Wall Street investor types would catch on to the revolution that has been ongoing in Peer to Peer Lending and crowdfunding and jump on the proverbial bandwagon. That happened back in April 2010 with Mikael Rapaport's creation of Peerform, the New York City-based Peer to Peer Lending platform. As with rivals Prosper and Lending Club, Peerform does not do any lending directly from its own coffers. Rather it puts borrowers and investors together on its own Online platform.

Peerform Intro & Background

While Peerform did not manage to become as wildly successful as its two larger and more powerful rivals after its initial hopeful launch, it has recently re-tooled the model it delivers in order to transform into the option for borrowers who lack terrific credit. As such, it is able to market itself well to investors as a higher-paying chance to earn a stellar rate of return of 9.88% (in 2014) at the same time when larger and better known original P2P lender Prosper only reported 6.87% returns.

The firm itself was created by a group of executives from Wall Street who possessed backgrounds in both technology and finance, an unusual combination. The founding motivation centered around their clear observation that the traditional lenders had become unable or unwilling to help small businesses and people. They saw that while interest rates remained historically at all time lows, money did not flow into the nation's economy as it was supposed to and was needed. Because of this, the group of Wall Street investors banded together to address the critical shortage of funding to individuals and small businesses and created a platform for marketplace lending with two principle goals. They wanted to offer borrowers an uplifting experience for getting personal loans in a procedure that was not only fast and clear, but also fair. Their other goal became to provide a well-checked out choice for investments in a loan portfolio that would give investors the opportunity to gain superior returns adjusted for risk.

We found that they actually do accomplish both of the goals. This platform is therefore best for individuals who are facing down financial difficulties, need to refinance their personal or small business debt, or who have recently experienced a life-changing event. The company Peerform has done well enough at this to garner quite a bit of attention from the media in favor of its platform and strategy. They have already been featured in Time Magazine, on Lend Academy, and on Alley Watch. Part of the reasons for their great success so far can be attributed to their no secret or no hidden fees policy. Borrowers are only required to pay Peerform basic origination fees when they take out their loan, so long as they make their full loan payments on time every month. Because their online platform is actually much cheaper to operate than a physical location brick and mortar traditional lending institution, Peerform has been able to pass along the savings to its lending clients and borrowers using a transparent method.

Peerform Founder and Management Team

Co-Founder and CEO Mikael Rapaport is the driving force and original creative mind behind Peerform. As original CEO, he has led and guided his startup to considerable success and positive reviews. Before leaving to start Peerform, Mikael served as the Head of Structured Credit Derivatives at Cantor Fitzgerald, one of the global bond trading financial services firms that also specializes in asset management, investment banking, brokerage services, market making, and market data. Prior to this post, Mikael held jobs at ICAP North America and also Bear Stearns, where he was trading structured credit products.

Co-Founder and CTO Meytal Benichou manages all of the IT functions for Peerform. Among her responsibilities are infrastructure, development of applications, design, and security. Before this company which she helped to found, Meytal served with Societe Generale in the New York office working on an important technology initiative for the fixed income business and equity derivatives product lines. She has a Master of Science degree from the Ecole Nationale Supérieur des Télécommunications in Paris in the field of Computer Science and Information Technology.

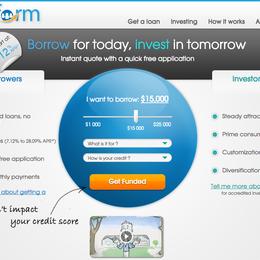

Peerform Loans

With Peerform, you are able to borrow from $1,000 on up to $25,000. The maximum amount is fairly typical for these types of unsecured personal or small business loans, but the lower number is unique and helpful for individuals who really only require a smaller loan. Peerform distinguishes itself from many of its P2P peers by breaking with the traditional up to five year loan repayment programs, only offering a single three year repayment term. This raises the amount of the monthly repayments considerably as compared to those five year repayment term loans. Prepayment penalties are not an issue, meaning that you can pay back extra whenever it suits you in order to reduce or even eliminate the balance early.

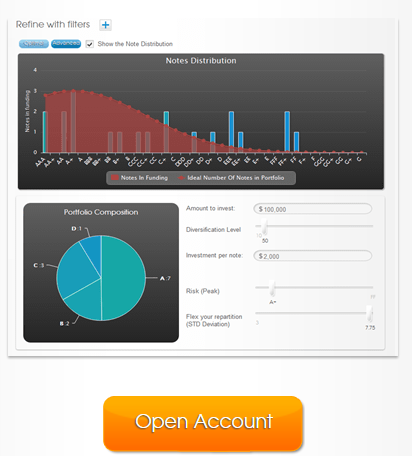

Peerform presently provides two different investment products and vehicles for investors to participate in, Whole and Fractional Loans. The whole loans are larger by nature and are intended for the institutional investors. Fractional loans are pieces of loans and are created for the individual investors, who for now must still be accredited, at least until early January 2016 when the new JOBS Act Title IV section comes into effect through the SEC.

Peerform is determined to allay any concerns from investors and potential investors regarding the continuity of the platform's servicing and operations. They established a partnership with the leading custodian in the industry and also with a backup servicer that possesses a well-proven track record of success to ensure that should anything befall Peerform, all payments on existing loans will still be collected and all payments due to investors will continue to be made seamlessly and without any interruption.

How Peerform Works

Peerform distinguishes itself from the myriad of P2P lenders by requiring less onerous standards of its prospective borrowers. Their rates are fixed for the life of the loan, which is different from some of the rival platforms too. With a credit score of only 600, borrowers will be seriously considered for a personal unsecured loan. Most of the rivals in the Peer to Peer lending space require a minimum of 640 to 660 and higher. The successful borrowing candidate also may not have a debt to income ratio that is at or higher than 40%, nor possess any records of tax liens, bankruptcies, judgements, or have any delinquencies on their credit reports.

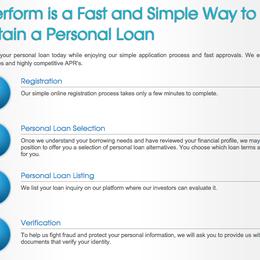

The process of getting loans approved, listed, and invested in on the platform is both intuitive and straightforward. Borrowers begin it by setting up an account, where they answer basic informational questions about their name, address, phone numbers, and salary. The Peerform platform then takes this information and analyzes it, simultaneously performing a soft hit on your credit report. This way, borrowers are able to obtain information on their approval status and an interest rate on the loan without having to take a hard hit on their credit report.

After approval, this loan marches on to its listing on the database and platform. Investors await it here so that they can fund it fractionally or in whole. It requires as much as 14 days to process the funding and loan disbursal of funds. In 14 days, if there is insufficient interest in the loan from the site's investors, then the application is pulled and rejected. Cross River Bank, the FDIC-insured New Jersey-based and -chartered bank processes this platform's loans, as it does with several other P2P Lenders.

Investors from all fifty of the U.S. states may participate in the platform P2P Lending, but borrowers are not so fortunate at this point. The company's loans are only permitted in Washington, Virginia, Texas, Tennessee, Oregon, Ohio, New York, Nevada, New Hampshire, North Carolina, Missouri, Minnesota, Michigan, Maryland, Louisiana, Illinois, Hawaii, Georgia, Florida, Connecticut, California, Arizona, Alabama, and Alaska.

Peerform Services

- Loan Grading – Loans are assigned grades based on the credit soft pull. This grade impacts many elements of the loan and on the platform, including maximum amount of the loan, origination fee amount, and loan amount total. The loan grade will also determine at what investment rate the note pays when it is picked up by one or more investors on the platform.

- APR Rate Determination – The company's APR starts from as low as approximately 7% and goes up to as high as about 28%. This is actually lower than practically every competing service in the peer-to-peer lending space.

- Peerform Loan Analyzer – This proprietary algorithm is both dynamic and very advanced. It is employed to set the pricing on the loans and represents a new technological standard in the P2P Lending space.

- Empirical Calculation of Credit Risk – Thanks to this leading technology algorithm, constantly being improved upon, Peerform is able to work with empirical methods instead of filters to better and more exactly determine risk from consumer credit. This allows the platform to bring on more borrowers using pinpoint accuracy pricing as compared to their traditional rivals in the consumer lending space. It is another fantastic level of value for investors who feel more confident in the interest rate versus risk that they are accepting.

- Portfolio Builder – Thanks to Peerform's superb ability to diversify, you can set up a consumer and small business loans portfolio which helps to better diversify your traditional stock, bond, and real estate portfolios you have elsewhere. This is accomplished using the platform's one of a kind portfolio builder to establish a portfolio that matches up with your risk-tolerance in your profile on the site.

- Goal Setting Customization of Portfolio – Once you set up your goal for rates of return, the platform's customization tool will instruct you on where and how to deploy your capital on the site so that you can reach your return objectives in the best consistent and dependable manner.

- Stable and Appealing Returns – This marketplace provides you with the prospect of appealing returns that are adjusted for your personal risk tolerance and provide a dependable monthly cash flow that is directly deposited straight to your personal bank account.

Peerform Locations

Peerform has one thing in common with many of its P2P space rivals. It maintains a single office in New York City. Their corporate headquarters can be found at 33 West 17th Street, 2nd Floor, New York, NY 10011.

Peerform Interface Screenshots

Peerform Safety

Peerform is imminently concerned with the safety and security challenges that face this booming industry. To that effect, they have instituted high-tech Fraud Prevention Systems. This involves their combination of in-house intellectual designs, commercially vended technologies, and other creative and effective solutions in the marketplace to prevent fraud by detecting it early. The security team deploys techniques like KBA Knowledge Based Authentication, specifically designed software that augments their own fraud detection efforts, and behavioral analytics.

Besides this, they employ many third party services to help ensure that user identification is done properly, with Lexis Nexis handling id's, credit checks performed by TransUnion, and compliance managed by OFAC standards. Cases that the algorithm or protocols flag as high risk for fraud are verified using both employment data and income sources and documentation as each borrower is required to report. Peerform states that it costs a great amount of time, energy, and resources to enforce and police this zero tolerance fraud policy, but they believe it to be an urgent priority for the site and platform. They claim that their procedures and protocols are among the most aggressive and strict in the space so that they can vastly reduce the risks of fraudulent loans to their investor base.

Peerform Complaints and Ratings

The Better Business Bureau maintains its highest rating of A+ on Peerform. It earned this coveted ranking because of the amount of time the company has been operating (over five years) and because there are presently no complaints at all filed against them with the BBB. This is a significant achievement in customer service to have zero complaints registered with the BBB after five years of operations.

Peerform Customer Support

The company is free with revealing its phone number and email address. We contacted them both ways to discover that their customer support is positive in both channels. Email gained a response on the following day with the answers to most of the queries that we posed. Regarding phone support, the customer service rep with whom we spoke demonstrated clear and commanding knowledge of the loan process and business. Besides this, Peerform also offers a good live chat service on the platform and site. The site itself adequately discloses information and operations of the company and its loans, such as APR's, rates, potential costs and loan sizes, and all that you need to know about the application process itself.

Peerform Costs & Fees

The costs on Peerform are clear and transparent for both borrowers and investors. Investors pay nothing to participate and have their portfolio managed, with information and updates on loans provided. Borrowers pay only origination fees and interest rates, assuming that they keep up with their monthly payments. The origination fees range from 1% to 5%, although this is part of the APR rate which is payable upfront in a lump sum that is simply deducted from the amount of the loan itself. This means that borrowers who have a targeted and specific need should include the cost of the origination fees in their calculations.

The rates are determined using the smart algorithm that places borrowers in a Peerform grade which ranges from AAA at best to DDD at worst. The best interest rates are doled out to the AAA-grade rated borrowers naturally, while the DDD-graded borrowers can expect to pay the very highest rates the site offers. The only other fees are set at industry standard levels. These include $15 returned payment fees and late fees that are either the greater of a $15 charge or 5% of the loan payment in question.

Final Words on Peerform

Peerform has much to recommend it to both borrowers and investors. The application process for borrowers is quick and simple. The loans provide a fixed interest rate to their borrowers, so that there is no change to monthly payment amounts. Their interest rates are more or less competitive with their rivals, though they can be a bit higher than the majors in this P2P Lending space. This is the price that you pay to have less rigorous requirements and easier minimum qualifying standards so that borrowers with credit scores at 600 and up are able to apply. The lower minimum loan amount of $1,000 does not require a credit check, which is nice for borrowers who need a smaller amount.

While the process of obtaining funds with Peerform may take a little longer at up to 14 days to process, fund, and disburse the loan, the amounts that they are loaning out unsecured as personal loans are good at from $1,000 to $25,000. For individuals whose credit is imperfect and who wish to avoid interest rates that exceed 30%, Peerform is a good and timely solution to the age old funding problem.

Peerform

- Phone : 1-800-388-8049

- URL :

- Global Rating

- Good

User Rating

- 0 No reviews yet!

Review Summary :

Peerform has found a desperately needed niche in the under-served, 600 credit score borrower market and has built a successful Peer to Peer Lending business model on this group. Thanks to their cutting-edged proprietary algorithm, they are able to accurately price risk and return factors in the P2P lending equation. Their investor interest rate returns are better than those of their main rivals in the space, making this a very attractive platform for investors who want to diversify their holdings into a personal and small business loan portfolio.

Have you purchased products from Peerform? Leave a review!

Gold: $2,387.15

Gold: $2,387.15

Silver: $27.92

Silver: $27.92

Platinum: $931.67

Platinum: $931.67

Palladium: $903.43

Palladium: $903.43

Bitcoin: $67,909.13

Bitcoin: $67,909.13

Ethereum: $3,254.68

Ethereum: $3,254.68