- GOLD IRA

- Download Our 2024 Precious Metals IRA Investor’s Guide.

Click Here

Gold IRA

Gold IRA

- Investing

-

- CRYPTO IRA

- PRICES & STATS

- RETIREMENT PLANS

Questions? Call (888) 820 1042

Questions? Call (888) 820 1042

Silver

Silver Gold

Gold Platinum

Platinum Palladium

Palladium Bitcoin

Bitcoin Ethereum

EthereumPave Review

Disclosure: Our content does not constitute financial advice. Speak to your financial advisor. We may earn money from companies reviewed. Learn more

Last Updated on: 25th March 2023, 12:07 am

Review Summary :

For a Peer to Peer Lender that makes unsecured personal loans to younger, less qualified borrowers, Pave fills a critical need for their customers. Lenders may have some reservations about handing over a large amount of money to invest in the unsecured loans when the information provided on their website and platform is less than transparent and many questions remain unanswered by the site.

Pros:

- Some of the lowest origination costs of any P2P Lender or traditional lender.

- Very reasonable criteria to qualify for one of their unsecured loans.

- Simple to utilize website and platform.

- Customer service is friendly when available.

Cons:

- Time for funding a loan takes a little longer than average for this industry, at typically four days.

- Customer service can be hard to reach when you need them.

Quick Facts about Pave

Reviewed By:David Crowder

Have you purchased products from Pave? Leave a review!

Peer to Peer Lending is no stranger to competition. Among the numerous companies popping up to make unsecured or real estate loans to individuals or businesses is Pave P2P Lending based in New York City, NY. What makes them different is their more creative approach to loan underwriting, as well as the interesting background of their founders, management, and staff. Their team of dedicated professionals mostly got their stripes at many of the best known technology and finance companies around the globe, such as Facebook, Apple, American Express, Microsoft, Visa, and Goldman Sachs.

Pave Intro & Background

Pave's mission and motto is to eliminate the biggest obstacle to success that younger people face— the lack of access to funding that is affordable. They began this quest by offering the Pave Loan. Their technology allows them to provide the most economical loan rates to young people. They do this all the while looking past just their credit report and score to see who they are as people of potential and where they are headed in life.

Investors and backers of the Pave Loan program and platform are those who believe in investing in the up and coming generation. They choose loan portfolios to fund and then are repaid over a two to three year time frame. This creates a definite win-win situation for both younger borrowers and older, more stable financially, and better financed investors.

Pave Founder and Management Team

Pave's core team is small but highly energized. Professionally they hail from American Express, Apple, Facebook, Goldman Sachs, Visa, and Microsoft.

The Co-founder & CEO of Pave is Oren Bass. Before starting his P2P organization, Oren worked in Structured Finance for Goldman Sachs, and with Clifford Chance prior to that. He is also one of the Trustees at Fcancer.org.

Co-Founder Sal Lahoud is also presently the Chairman for Fcancer.org. He worked at GLG in media, film, technology, and special situations. Sal has a varied educational background as he studied English at Imperial College and Theater at Esper Studio.

Head of Product and Operations Ray Tamblyn also co-founded PayDivvy and headed up V.me by Visa. He remains passionate regarding innovation, design, and product.

Pave Loans

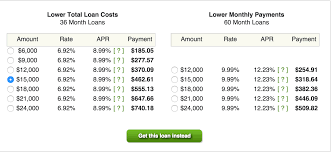

The loans at Pave are available at from $3,000 to $25,000 and carry APR's of from as low as 6.5% on up to 20.29%. Repayment terms range from between two and three years.

While the origination fees that come with the Pave loans are some of the lowest around, the interest rates can be a little higher than some rivals. The company considers more than simply credit history and scores, though this is an important criteria as the platform has a minimum credit score requirement of 660 to qualify. Pave loans are available in 35 of the states. For those who reside in Wyoming, Wisconsin, Vermont, Tennessee, Pennsylvania, Oregon, North Dakota, North Carolina, New Jersey, Nevada, Nebraska, Massachusetts, Maine, Connecticut, Arizona, and Washington D.C. they are out of luck at borrowing money from Pave, as are the investors in these states who would like to participate through investing.

One interesting and unusual statistic that Pave touts is the purpose for the borrowed funds. Sixty percent of Pave borrowers claim that they will deploy the funds to further their careers. The other 40% plan to consolidate debt or refinance at a better, more competitive interest rate that the platform offers its borrowers.

How Pave Works

Pave determines the interest rates that its borrowers receive utilizing a variety of factors, some of them unusual and beyond the scope of traditional loan underwriting criteria. They do start with the borrower's credit score. It has to be at least 660 to apply. Fortunately for many younger borrowers who are not yet well-established in careers and income, they do not maintain a fixed limit on debt to income ratio.

For investors who are interested in getting in on the opportunity presented by up and coming millennials, you gain principal plus interest payments as the borrowers repay their loans over a two to three year period of time. The downside is that the interest rate return is not as high as with many of Pave's competitors. This is because the Pave loans are actually lower risk than those loans that many of their competing platforms offer. The upside to these types of loans centers on the fact that the investments are stable and have lower default rates than with some Peer to Peer Lending companies.

Pave Services

Pave does not offer so many services as some of its larger and more established rivals like Lending Club and Prosper, but it does provide the essentials.

- Loan Servicing Partnership – Pave has a partnership with a leader in the servicing industry that helps it to collect on loan payments and outstanding loan amounts. In the event of a default, they will terminate the installment agreement and attempt to work with this partner to recover the initial principal amount minus the payments of principal that have already been made.

- Payments and Servicing – The experienced professionals at Pave have designed their own proprietary servicing and payment system for collecting monthly payments. This utilizes standards that are already established in the industry with its state of the art technology.

- Contingency Plans for Operations – Should Pave fail or go into bankruptcy, they have already made contingency plans with a back up servicing company that possesses in excess of 40 years worth of experience at servicing a book of loans valued at more than $9.4 billion. Since the loan servicing terms are identical to those already in place with the current servicing arrangements, investors would not suffer any change in their payments or fees in the event of a necessary but smooth transition.

- Create a Personal Loan Investment Portfolio – All that you have to do is to sign up on the website, create your user profile, and then choose a portfolio in which you are interested. After you have finished with these simple tasks, the Pave team members will contact you to help you with the next steps.

- Holistic Approach to Lending – Pave takes a more complete view of each borrower's individual situation than does a traditional finance company or bank. They go beyond credit history and score to consider other elements such as work history, intended use of the funds, present employment, educational history, and anticipated earning potential for the future. This way they can evaluate the level of financial responsibility a prospective borrower exhibits, and set the interest rate for repayment accordingly.

- Collections of Bad Loans – If loans in a portfolio that you are backing go bad, Pave and its servicing company will make all reasonable efforts to recover the principal on the loans for the good of all investors involved in those loans.

Pave Locations

As with most of the P2P lenders, Pave operates a single office. Their New York based headquarters can be found at 200 Varick Street, Suite 802, New York, New York 10014.

Pave Interface Screenshots

Pave Safety

The company promises that both private and other personal information will stay private and only be utilized to provide you their investors or borrowers with the highest possible level of service. Only you can change your account settings and purpose to use information on their platform.

Where safety of your bank data and other sensitive financial and personal information is concerned, Pave employs bank standards of security to protect your data. This includes industry standard encryption of credit card, bank card, and other personal financial data when it is both transmitted through the Internet or stored on their disks. All of their systems for card processing are kept to the Level 1 PCI Data Security Standards.The company's API and website can only be viewed using their 256 bit SSL certificates as provided by Network Solutions DV Server. Firewalls similarly safeguard all inter-network connections.

Regarding the storing of your money, Pave has a set of protocols for this as well. They keep all of your funds and those of the other customers safely in Wells Fargo Bank FDIC-insured accounts. All of their platform applications they develop themselves in-house and consistently test them for security in regular reviews.

Pave Complaints and Ratings

The company is newer (founded in 2012) so we did not find any BBB file or comparable ratings. Credit Karma reviews are mostly positive on the company so far, which is encouraging if you are considering buying into some of their unsecured loans. We did not find other complaints when conducting our online search.

Pave Customer Support

Customer service is a mixed bag with Pave. On the one hand, they do publish their phone number on the home page, and also give out two different email addresses on their contact us page, as well as have a contact form. The company also provides a frequently asked questions section, though it is a bit thin on the responses they provide to answer the queries.

The company is rumored to have a live chat feature, though we did not find it on their contact us page. Actually contacting the company proved to be a little frustrating. An email sent in with basic questions did not garner a response. They did answer the toll free phone number and were more helpful with this avenue of contact.

Pave Costs & Fees

Pave charges origination fees to help cover their costs and make money. Their origination fee has been fixed at 2%, which is significantly lower than many of their competitors who charge anywhere from 1% to 5%. Check processing fees come in at $2, considerably lower than most rivals who get $15. Late fees are standard for the industry at the higher amount of either $15 or 5% of the late and overdue amount.

Final Words on Pave

One hidden asset that Pave boasts is the big time names of a few of their advisors. Laura D’Andrea Tyson was an advisor to President Bill Clinton. Samir Assaf heads the British banking giant HSBC's Global Banking and Markets division. These major names would not be involved or have their names associated as advisors to a fly by night or slipshod organization. The APR's at Pave range from average to on the high side, while the origination fees at 2% are low for the industry.

The biggest concerns we have with Pave concern the lack of transparency and information provided on their website, which is at the heart of the entire platform on a P2P lending operation such as theirs. The site fails to properly and sufficiently explain the investing process or even to adequately answer simple questions. Customer service is available, though not as quick as an investor whose hard-earned money is on the line would want. It sure would be nice to know what the average returns and loss rates are for their various portfolios of loan holdings too.

Review Summary :

For a Peer to Peer Lender that makes unsecured personal loans to younger, less qualified borrowers, Pave fills a critical need for their customers. Lenders may have some reservations about handing over a large amount of money to invest in the unsecured loans when the information provided on their website and platform is less than transparent and many questions remain unanswered by the site.

Have you purchased products from Pave? Leave a review!

Gold: $2,387.15

Gold: $2,387.15

Silver: $27.92

Silver: $27.92

Platinum: $931.02

Platinum: $931.02

Palladium: $903.43

Palladium: $903.43

Bitcoin: $67,910.26

Bitcoin: $67,910.26

Ethereum: $3,278.81

Ethereum: $3,278.81