- GOLD IRA

- Download Our 2024 Precious Metals IRA Investor’s Guide.

Click Here

Gold IRA

Gold IRA

- Investing

-

- CRYPTO IRA

- PRICES & STATS

- RETIREMENT PLANS

Questions? Call (888) 820 1042

Questions? Call (888) 820 1042

Silver

Silver Gold

Gold Platinum

Platinum Palladium

Palladium Bitcoin

Bitcoin Ethereum

EthereumMonte Paschi Problems to Persist After Bailout as British Consumers Hoard Cash and Fed Becomes Constrained

Disclosure: Our content does not constitute financial advice. Speak to your financial advisor. We may earn money from companies reviewed. Learn more

The last week of 2016 saw more of the customary turbulence which has become so commonplace in a market-rocking volatile year. Italy's Monte Paschi Bank may be getting an over 8 billion euros bailout, yet the European Central Bank forecasts their problems will continue indefinitely following the latest fresh capital infusion. Meanwhile, the higher capital reserves bar which the central bank has set for Monte Paschi would cause 10 other European banks to come up lacking in sufficient capital. The British are hoarding their cash while they wait to hear the upcoming details on the Brexit strategy which will be triggered by March. All of these events are constraining the Federal Reserve's abilities to implement the three additional rate increases they have announced as part of their New Year's Resolutions for 2017. It all argues for you to add approved gold to your self directed IRA account.

Shocking News Emerges that Monte Paschi Bank's Troubles Post Bailout to Persist Indefinitely

It is now front page news the world over that troubled third largest Italian and oldest in the globe lender Monte dei Paschi di Sienna Bank is to receive over 8 billion euros in a state-sponsored Italian government bailout. The tragedy is that this is not going to solve the bank's ongoing problems, but will only buy the embattled Italian lender more time to try to sort out what it has been so far unable to do since 2008, nearly a decade ago. The interim Italian Prime Minister Paolo Gentiloni let slip Thursday that the Monte Paschi recapitalization will prove to be both “long and complicated” even as it is necessary for the institution and the Italian banking sector to survive.

The European Central Bank has upped the proverbial ante by shock announcing that the Italian Monte Paschi Bank actually needs 8.8 billion euros, or around $9.2 billion US dollars, to sufficiently stabilize its continuously deteriorating financial position in the banking universe. The bank had told analysts and investors it only required 5 billion euros, or $5.4 billion US dollars, to effectively be saved. The bailout will begin in the first three months of the new year 2017, yet it does not stave off growing concerns for the overall Italian banking system, the political future of Italy, and even for the overall eurozone and troubled banks. The ECB determined the larger capital requirement after watching the capital flight of depositors withdrawing their funds from the banks' accounts in a slow motion-like bank run. This has caused the group's finances to rapidly deteriorate even further in the past month. Economy Minister Padoan argued that the now 8.8 billion euro bailout of the bank will ensure that the world's oldest lender becomes “hyper capitalized” yet not “over capitalized,” per a report from Reuters.

The biggest danger at this point is delayed effective bailout action. If the Italian politicians and banking regulators drag their collective feet on the intervention, Monte Paschi's stability will deteriorate still more. Padoan and the Italian provisional government have already ruled out delisting the bank from the Milan-based Italian Stock Exchange. The real question now is whether the Italian government's approved 20 billion euro bailout funds will still be sufficient to help out all of the other troubled Italian financial institutions give that they are having to pour in nearly 4 billion additional euros to Monte Paschi beyond their original plans.

The Italian treasury reported via Reuters last week that the earmarked 20 billion euros should be sufficient to “revamp the ailing banks.” As Italy (and Germany and France) are heading for new elections in the coming months, the process is quite delicate and most important to proceed as smoothly as possible. German politicians have already begun calling for the European Commission to disallow this particular state banking aid package as illegal.

Ten Other European Banks Would Fail New Capital Requirements Imposed on Monte Paschi Bank

As if the financially perilous Italian banking situation revolving nervously around Monte Paschi Bank was not scary enough, the ECB's latest elevated capital requirements for the financial institution raise another troubling spectre. According to these rigorous and more capital intensive requirements, the ECB is indirectly implying that fully 10 other continental banks would be in financial trouble as well. The names of fellow banks that are now unofficially on the capital watch list are substantial heavyweights from some of the wealthiest countries and financial centers on continental Europe. These include Germany's largest lender Deutsche Bank, Italy's largest bank UniCredit, and eight other European financial institutions including Allied Irish Bank in Dublin. None of these would boast sufficient capital to meet the ECB's particular requirements now expected of Monte dei Paschi if new stress tests were run at these significantly higher levels.

The European Central Bank has informed Monte Paschi that it will need to have sufficient capital on hand to move up its Tier 1 ratio to fully 8 percent of the total risk-weighted assets in order to pass the worst case stress test scenarios, per the statement on December 29th from the Bank of Italy. This new and improved 8 percent requirement is considerably higher than the legal minimum capital reserve ratio of 4.5 percent. Even the 2014 stress tests only insisted on a 5.5 percent capital ratio.

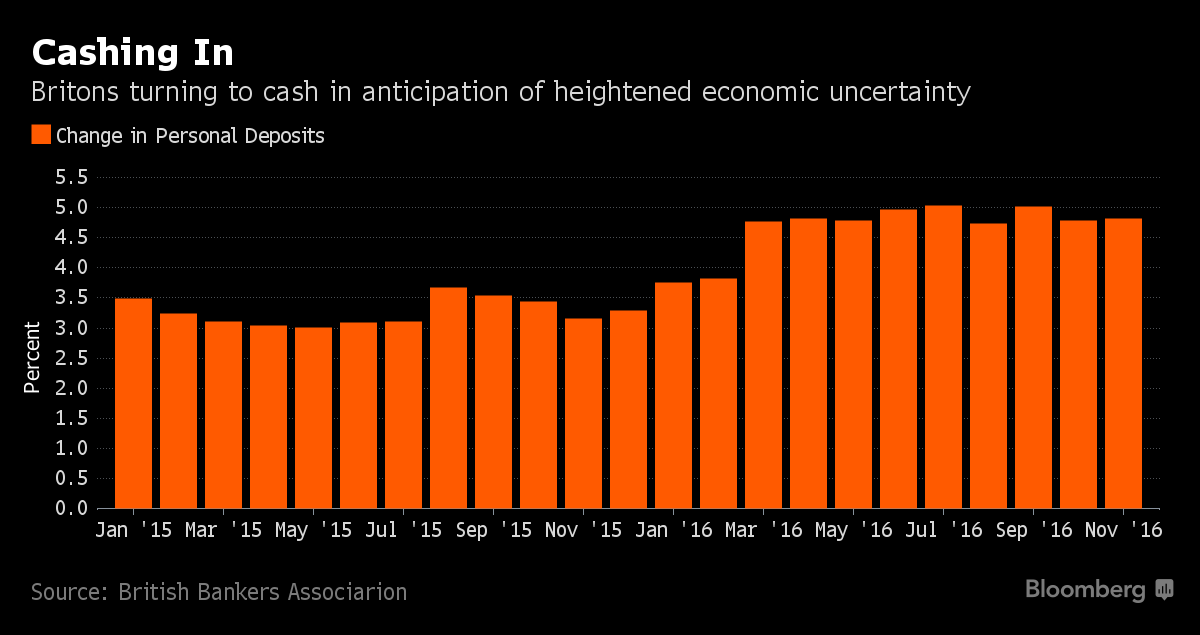

Unconfident British Public Hoarding Cash Ahead of Brexit Details News

It is no wonder that with all of the problems for European banks across the channel that the British are choosing to hoard cash rather than spend it. This trend began in the months preceding the Brexit referendum vote and has only escalated since then. The British Bankers Association this past week revealed that the British public is holding on to its cash in their latest proof that they are worrying about the economic uncertainties ahead in 2017 with the Brexit negotiations due to start in March. This is most evident in the annual growth of the personal deposits, which increased by 4.8 percent for November. For the first 11 months of 2016, these deposits grew by a staggering 32.4 billion pounds (or $39.7 billion US dollars) versus the prior 11 month period of 2015's 19.8 billion pounds. This chart demonstrates how the savings rate has been on the move in the second half of 2016 especially:

Even though the British economy has so far held up better than economists initially expected, most economic analysts foresee some type of a slowdown for 2017 while businesses await details on the future of the U.K. as it relates to trading with the biggest trading block on earth in the remaining members of the E.U.

Fed Easing for 2017 Seen As Constrained By The Rest of the World's Central Bank Policies

Since it managed to finally increase its benchmark lending rate a mere one time at the end of 2016, the U.S. Federal Reserve has been talking up a good game about its “New Year's Resolution” to raise American interest rates by three more times in 2017. This aggressive claim in December took both economists and analysts by surprise. Yet per the economists at world's largest international bank (by balance sheet) British multinational group HSBC, the U.S. central bank will find itself “constrained” on raising interest rates so many times in the new year. Global Economist at HSBC James Pomeroy stated, “We're…of the view that the fed is constrained by not just its own inflation outlook, it's constrained by wage growth but it's also constrained by the rest of the world. And actually if you're in a world where as the Fed sort of continues to raise rates that you get a stronger dollar, that sort of hurts the emerging world, and actually that's a situation that will constrain what the Fed is able to do.”

It is certain that the Fed must consider many diverse criteria which impact not only the U.S. economy, but also economic conditions for the rest of the world. Among the factors that tied its hands in 2016 were the various troubling geopolitic such as the Chinese growth story, the Brexit surprise “no” referendum vote, and the shocking American election results. For the year 2017, the Fed must contemplate its actions and their indirect consequences for election results in Germany, France, and Italy; the critical Brexit negotiations; and what its policies will do to growth in China. It is also unclear how much President-to-be Donald Trump's promised policies on infrastructure spending, tax cuts, and deregulation will have on their future decisions. Taking all of this into consideration, HSBC only foresees two actual rate increases for all of 2017. HSBC's Pomeroy feels that the year 2018 will prove to be “even harder” for the Fed. All of this is incentive for you to add gold to your retirement precious metals IRA in the new year.

Gold: $2,387.15

Gold: $2,387.15

Silver: $27.92

Silver: $27.92

Platinum: $931.02

Platinum: $931.02

Palladium: $903.43

Palladium: $903.43

Bitcoin: $67,910.26

Bitcoin: $67,910.26

Ethereum: $3,278.81

Ethereum: $3,278.81