- GOLD IRA

- Download Our 2024 Precious Metals IRA Investor’s Guide.

Click Here

Gold IRA

Gold IRA

- Investing

-

- CRYPTO IRA

- PRICES & STATS

- RETIREMENT PLANS

Questions? Call (888) 820 1042

Questions? Call (888) 820 1042

Silver

Silver Gold

Gold Platinum

Platinum Palladium

Palladium Bitcoin

Bitcoin Ethereum

EthereumLoosening Dodd-Frank Act Threatens Another Banking and Financial Crisis

Disclosure: Our content does not constitute financial advice. Speak to your financial advisor. We may earn money from companies reviewed. Learn more

Last Updated on: 31st August 2021, 12:47 am

Last Wednesday, you saw the Senate pass legislation that eased tough banking rules. This bipartisan effort weakened the regulations that had been erected to keep a repeat of the Global Financial Crisis of 2008 from occurring. Millions of Americans lost their homes, jobs, and savings in the now decade old crisis. Loosening these rules makes it that much more likely that another such financial crisis will roil American and global markets in the future.

This is a prescient reminder to you of why you need to hedge your investment and retirement portfolios with IRA-approved metals. It is true that gold makes sense in an IRA because it outperforms and stabilizes in times of market crisis. You should think about the top five gold coins for investors now while the markets are calm.

Changes to the Banking Law Worrying

The Dodd-Frank Act created tough standards on the individuals to whom banks could make loans and mortgages following the defaults of hundreds of thousands of home loans that led to foreclosures. These overturned the U.S. (and global) economy back in 2008. The flip side to such legislation was that once-reliable customers who suffered from financial setbacks in the aftermath of the crisis were no longer able to obtain loans.

This revised legislation is loosening up rules that have so far kept the crisis from repeating. A main change is that it increases the level at which banks become labelled too big to fail. Financial institutions at this size are crucial to the entire financial system. They wreak major destruction on the economy when they fail. Banks at this level undergo tougher planning and capital requirements.

Now Congressional lawmakers are working towards significantly loosening up these restrictions on banks in an effort to increase lending and build the economy. The Senate has just passed the new rules in a 67 to 31 vote that Republican Mike Crapo from Idaho introduced.

Dismantling the Dodd-Frank legislation has also been on President Donald Trump's agenda since he campaigned to be president. He has pledged to sign it after it positively passes both houses of Congress. The White House wrote in a statement following the successful Senate vote:

“The bill provides much needed relief from the Dodd-Frank Act for thousands of community banks and credit unions, and will spur lending and economic growth without creating risks to the financial system.”

The issue is that a number of critics feel that weakening the legislation sets up another banking and financial crisis in the future.

Critics Warn Legislation Gives Banks Too Much Power Again

It's not like banks are struggling to make money ten years after the last financial crisis. In fact they are now earning all-time high profits again. Advocates in the banking industry argue that the Dodd-Frank Act crushes tinier financial institutions that lack sufficient resources to adapt to it.

Yet there are a number of critics pointing out that the laws are necessary to stop the irresponsible behavior of the too big to fail banks. Massachusetts Senator Elizabeth Warren and Ohio Senator Sherrod Brown are two of these. Both feel that the new legislation panders to the banks that created the financial crisis in the first place. They worry that it will create another situation which requires bank bailouts from taxpayers.

Senator Brown shared his concerns before the vote took place with:

“Big banks and their lobbyists are about to score a touchdown at the expense of hardworking families across the country.”

One of the main changes in the bill is to increase the amount of assets a bank must have before it is considered to be a possible threat to the system (in the event of a failure) by five times. Now banks would need $250 billion in assets before they earned the label of too big to fail.

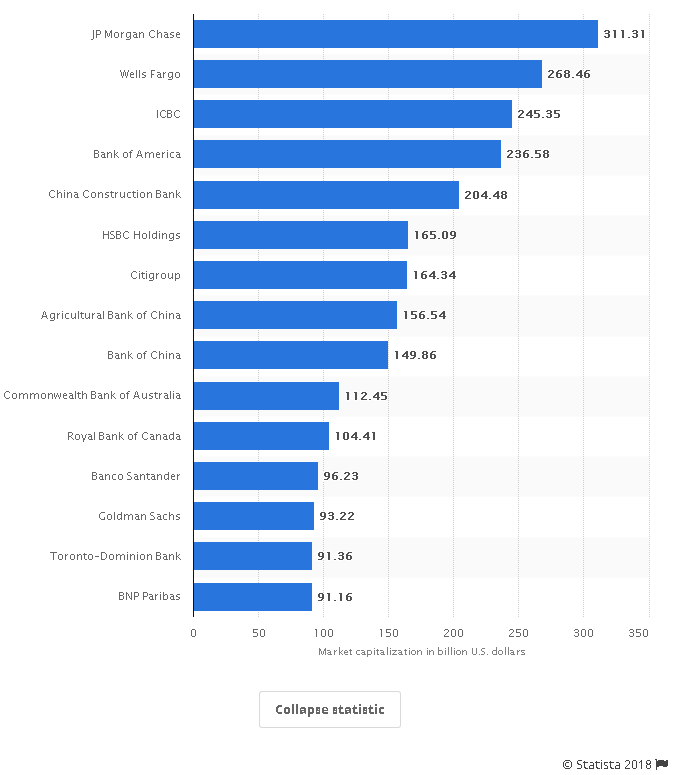

This would reduce the oversight and regulations on over 25 financial institutions throughout America. Among those receiving less restrictive treatment would be SunTrust Banks, BB&T Corp., American Express, and Fifth Third Bancorp. This chart shows the largest banks in America in 2018:

Exempted Banks Escape Stress Tests and Living Wills

The banks which join the exempted category would benefit in a significant way. They would not be required to go through the demanding ritual of yearly stress tests that the Federal Reserve has conducted since the conclusion of the Global Financial Crisis.

Such tests consider if the participating bank possesses sufficient amounts of capital buffers to successfully outlast a shock to the economy while still lending money to customers. Banks under the $250 billion asset level now will no longer have to create and provide their living will plans. These lay out the steps for the manner in which the bank would liquidate and sell its assets if it failed. It was designed to reduce financial system chaos when a bank fails.

Senate Committee Chairman Mike Crapo of Banking, Housing, and Urban Affairs defended the loosened banking restrictions. He made the point that the Federal Reserve would still retain the discretion to enforce the harsher standards on those banks that possess from $100 billion on up to $250 billion worth of assets.

Dodd-Frank Amendment Supporters Want More Lending

President Trump is among those supporting the amendment to the Dodd-Frank Act. He shared his thoughts on why with:

“We're looking now at Dodd-Frank because we have to free up so that the banks can loan money to great people, because they were restricted.”

Senate Majority Leader and Kentucky Republican Mitch McConnell feels that the Dodd-Frank Act was “too blunt” as a means of overseeing banks. He warned:

“Regulations meant for Wall Street are crushing Main Street.”

McConnell worries that it has kept the smaller financial institutions from making loans. These smaller lenders are responsible for over half of all small business loans and in excess of 80 percent of all farm loans.

Bill Increases Probability of Big Bank Failure

One group that it is hard to argue with is the non-partisan Congressional Budget Office (CBO). They have reviewed the amended legislation and have determined that it does somewhat raise the probability for a large bank failure. They note that this would increase the government deficit if it occurred.

The bill also eliminates other safe guards. Some credit unions and banks would no longer have to report their specific data on mortgage loans they make. Among this exempted information is the loan applicant's credit score, age, interest rate, and the costs of the loan. It makes it easier for benefiting financial institutions to engage in abuses without fears of banking oversight catching them.

Gold Protects Against Market Pullbacks from Bank Failures

As the CBO has pointed out, the loosening restrictions on Dodd-Frank allow for a greater chance of large bank failures. When the legislation becomes amended, we are that much closer to more disruptions in the financial system. The last financial crisis wiped out nearly half of the market value. It took years for the equities markets to bounce back to pre-crisis levels.

This is why IRA-approved gold is such a critical insurance component for your retirement portfolio. You can not control when another financial crisis breaks out. You can hedge your retirement portfolio against such an inevitable event. You can now buy gold in monthly installments, making it easier than ever to acquire. Now is a good time to consider Gold IRA storage options.

Gold: $2,387.15

Gold: $2,387.15

Silver: $27.92

Silver: $27.92

Platinum: $931.02

Platinum: $931.02

Palladium: $903.43

Palladium: $903.43

Bitcoin: $67,910.26

Bitcoin: $67,910.26

Ethereum: $3,278.81

Ethereum: $3,278.81