- GOLD IRA

- Download Our 2024 Precious Metals IRA Investor’s Guide.

Click Here

Gold IRA

Gold IRA

- Investing

-

- CRYPTO IRA

- PRICES & STATS

- RETIREMENT PLANS

Questions? Call (888) 820 1042

Questions? Call (888) 820 1042

Silver

Silver Gold

Gold Platinum

Platinum Palladium

Palladium Bitcoin

Bitcoin Ethereum

EthereumIs your nest egg large enough?

Disclosure: Our content does not constitute financial advice. Speak to your financial advisor. We may earn money from companies reviewed. Learn more

Retirement worries

In general people worry a lot about money, of course it depends on your age, the younger you are the more likely you are to be positive about the future and confident you are on track to becoming the next Rockefeller. GoBankingRates' 2015 Life & Money Survey finds that for 26% of American people money is what they think about the most. As we get closer to retirment age we still think about money, but now we are also concerned about making plans for retirement.

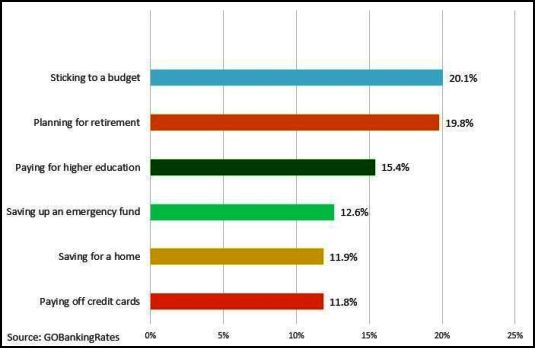

The current extremely high levels of the Stock market are causing great concern for those close to retirement. The worries don't finish there, other factors could prove to be a complication should there be another stock market sell off, such as a National debt exceeding $18.5 trillion, or the $11.9 trillion in Credit Card debt. The survey also finds that for 19.8% of Americans their biggest money challenge is planning for retirement, which is second only to sticking to budget which is the biggest money challenge for 20.1% of Americans.

Will I outlive my savings?

First figure out if you have enough to retire maintaining your current lifestyle. To do that you first need to calculate what percentage of your current income you are going to need as a retiree. This is called the replacement rate and varies greatly depending on your circumstances. Certain expenses are no longer made, for example commuting, but other expenses have to be taken into account in case of possible medical costs. It me be necessary to cut back on certain exepnditures to be able to live on your retirment savings and social security. According to the CNN Money retirment calculator, at age 50 with $400 thousand in savings and an annual salary of $100 thousand you need to save $25 thousand a year to be able to retire at age 67 and keep your level of income. That calculation is made taking into account living to the age of 92 and also factors in Social Security payments. However you also have to take into account you may live longer, and there may be higher than expected medical bills. Average life expectancy is still on the rise and it's feasible to think of reahing the low 90s but as we move forwad and medicine and health care continues to improve it may be wise to count on living longer than current expectations.

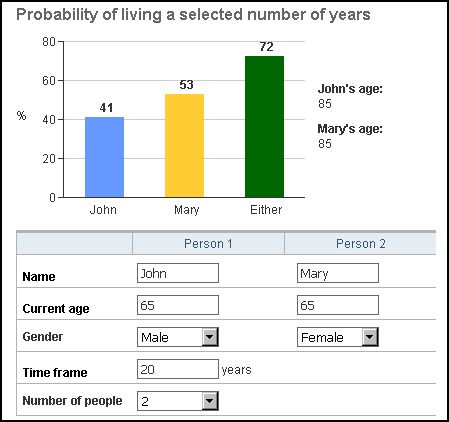

Life expectatancy for the US is at 78.7 years, although it is higher at 86.5 years if your Asian American and 82.8 if you are Latino. More than life expectancy alone its important to understand that we may live much longer than the average life expectancy. That average figure includes a lot of people who pass away before their time of other causes not related to age. According to Vanguard Asset Managers a couple that are currently both 65 years old have an 18% chance of at least one of them surviving to the age of 95. But if you look at the chance of a couple who are both 65 years old the chance jumps to 72% of at least one reaching that age.

The 4% Rule

This rule was studied in the 1990s and was simply the application of making withdrawls that start with a certain percentage. The studies found that an initial withdrawl of 4% and an increase every year by the rate of inflation would give a 70% to 80% chance of lasting 30 years. Let's say inflation is constant at 2% and your total savings are $1000,000, the first year you would withdraw $40,000 the second you would add 2% and withdraw $40,800 and so on. However some studies have found that due to the decrease in capital appreciation that we will likely see going forward for Stocks and Bonds it possible that a 4% withdrwal rate may find you running out of money well before last dance. David Blanchett tested in his study in 2013 for the probability of running out of money over a 30 year period. He tested for withdrawl rates that went from 2% to 8% based on different spending curves, with increments of 0.2. He finds that a 4% withdrawl rate with increments equal to inflation has a 73.3% chance of success. In another paper by D.Blanchett, M. Finke and W. Pfau the authors test the success rate of the 4% rule taking into account how markets might perform over the next 30 years. The study uses a performance estimate for bonds of 2% and a Stock market at 22 times price/earnings figure on a cyclically adjusted basis. It found that a portfolio with a 40/60 allocation to Bonds and Stocks had a 48% chance of success over 30 years with a 4% withdrawl rate. This study would seem to show how a small reduction in performance from Stocks and Bonds can seriously complicate our chances of applying even a modest withdrawl rate of 4%, bear in mind the Stock market price earnings ratio is currently at around 22.

This calculator by T.Rowe Price has a few more variables and needs a bit more detailed information. The biggest difference with this calculator is that it estimates the retirement income your capital might generate as opposed to the dollar value at retirement. The actual income generated is a more immediately comparable number that can allow you to have a better idea as to how well you are doing, and how likely you are to keep your lifesyle at retirement. It also allows you to play with savings rate, allocation size to Bonds and Stocks, amount of Social Security and other incomes.

Gold: $2,387.15

Gold: $2,387.15

Silver: $27.92

Silver: $27.92

Platinum: $931.67

Platinum: $931.67

Palladium: $903.43

Palladium: $903.43

Bitcoin: $67,909.13

Bitcoin: $67,909.13

Ethereum: $3,254.68

Ethereum: $3,254.68