- GOLD IRA

- Download Our 2024 Precious Metals IRA Investor’s Guide.

Click Here

Gold IRA

Gold IRA

- Investing

-

- CRYPTO IRA

- PRICES & STATS

- RETIREMENT PLANS

Questions? Call (888) 820 1042

Questions? Call (888) 820 1042

Silver

Silver Gold

Gold Platinum

Platinum Palladium

Palladium Bitcoin

Bitcoin Ethereum

EthereumBank of International Settlements Warns Higher Interest Rates Will Wreck Sovereign Governments

Disclosure: Our content does not constitute financial advice. Speak to your financial advisor. We may earn money from companies reviewed. Learn more

Last Updated on: 26th June 2017, 07:19 pm

Every so often, the Bank of International Settlements (BIS), appropriately based in Switzerland, comes out with their take on the global economy and their perceived risks to it. They recently published their latest one for the first half of 2017. Buried amidst their various warnings is one in particular that you need to be aware of, as it will affect the value of your retirement accounts and investment holdings in the not so distant future.

BIS' Ordinary and Routine Warnings

At casual glance, you might believe that the Bank of International Settlements is most worried about the unsettling geopolitical events of the last year that have overturned the post second world war order in the United States and Great Britain. The central bank of central banks (BIS) refers to this as the changing political landscape which has threatened the global economy. Among their highlights were the global implications from the shocking Brexit leave vote. Per the Sunday published annual report for 2017:

“Political events surprised market participants, who quickly needed to take views on the shifting policy direction and its economic implications. Attention shifted away from monetary policy, and political events took center stage.”

Yet this is only a theme they are hitting on among four significant economic and financial risks to the global economy. All or any one of them they say could threaten to derail the medium term expansion of the worldwide economic picture. As the report warns you:

“First, a significant rise in inflation could choke the expansion by forcing central banks to tighten policy more than expected. This typical postwar scenario moved into focus last year, even in the absence of any evidence of a resurgence of inflation.”

The BIS is also concerned about a weakening consumption and investment, financial stress from maturing financial cycles, and an increase in protectionism as a threat to global trade:

“A withdrawal into trade protectionism could spark financial strains and make higher inflation more likely. And the emergence of systemic financial strains yet again, or simply much slower growth, could heighten the protectionist threat beyond critical levels.

This is all intimidating sounding enough, yet it is still not the real danger which the Bank of International Settlements warns you about.

What Goes In, Must Eventually Come Back Out

Later in this report, the Bank of International Settlements finally gets to the point of the real danger that threatens the U.S. and global economies in a material way. Unfortunately, there is no easy solution or foreseeable fix for this threat. They explain that the world's foremost central banks lost no time whatsoever in flushing money through their economies in the wake of the disastrous global financial meltdown in 2008 and the 2012 sovereign debt crisis that rocked the euro zone.

There is plenty of blame to go around for these ensuing runaway expansionary monetary policies, and the BIS recognizes the most guilty parties. Among the institutions which rolled out dramatic bond buying programs and also drastically cut their interest rates in order to try to boost lending were both the United States Federal Reserve and the European Central Bank. The report singled them both out fearlessly.

Some central banks went so far as to force their national interest rates into negative for the first time in history. As a necessary consequence of this action, any bank in their economic jurisdiction was charged money to keep their reserves on deposit with the central bank. This applied in such central banks as the European Central Bank, the Danish Central Bank, and the Central Bank of Japan. There are severe consequences for this experimental and desperately irresponsible behavior, as the report soon hints at with its brief few lines warning about so-called “policy normalization.”

Policy Normalization Will Spell The End of Developed Nations' Solvency and Lead to the Dramatic Rise of Gold Prices

Policy normalization is a fancy central bank speak phrase for raising interest rates back up to historically normal levels. Already the U.S. Fed has pledged an end to easy money. This all sounds good and well, until you take into account the warning from the BIS report:

“Policy normalization presents unprecedented challenges, given the current high debt levels and unusual uncertainty.”

“Current high debt levels” is a euphemism for unsustainable debts on which the governments in the Western world can barely afford to make interest payments as it is. “Unprecedented challenges” is their way of saying that the governments who have engaged in these irresponsible actions will not be able to reverse them without potentially permanently wrecking their national governmental finances in the process.

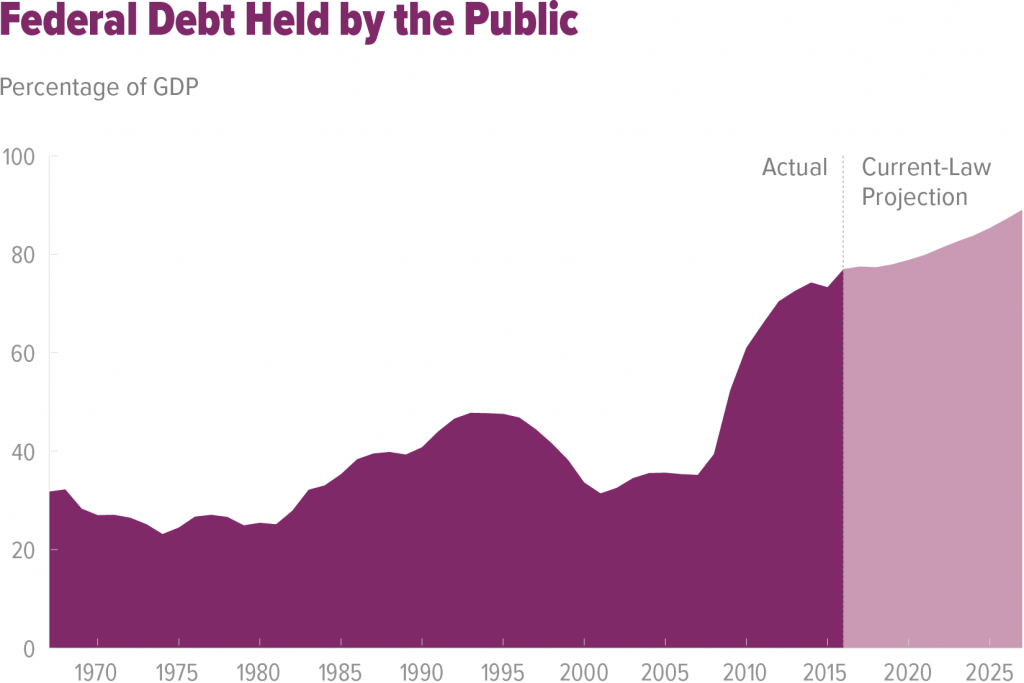

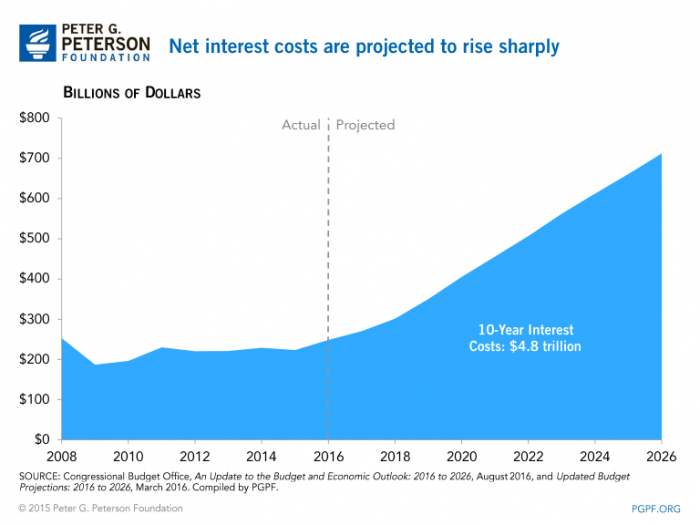

This is not a far-fetched conspiracy theory of a radical right or left wing group, but instead it is the warnings presented by the United States' very own CBO Congressional Budget Office in their recent findings. At present, the Federal Government of the U.S. pays $400 billion each year on maintenance interest only for the more than $20 trillion in American government debt.

But wait, it gets better. This hefty amount of interest is only applicable with interest rates at under one percent. The BIS is not alone in warning about higher interest rates in the future cards. The CBO ominously concurs with them on this inevitable eventuality (which has already begun with the Federal Reserve now raising rates three times consecutively).

What makes this most alarming for the future of the financial solvency of the United States is that every one percent interest rate increase means that the Federal Government's interest amount increases by another $200 billion per year. So when the Federal Reserve boosts rates by just one percent, they will jack up the American government's interest tab to a total of $600 billion.

It similarly means that with two percent greater rates, they will have to find another $400 billion per year. As you can already see, this devastating math only gets progressively worse as the interest rates continue to be raised back to normal levels. If they up the interest rates by three percent, they will need another $600 billion each and every year.

And by reaching the historically normal interest rates of just five percent, via increasing the rates by four percentage points, they will require an additionally ruinous $800 billion each year. The Congressional Budget Office itself puts these numbers out every so often, as this chart clearly warns:

It is important to remember that the American government brings in just over $2 trillion each year in taxes. Now this may sound like a vast sum to you and me, yet it is not nearly enough to fund the currently sized Federal government and all of its many entitlements, defense spending, welfare, and other social programs.

Beyond this considerable tax haul each year it already overspends a consistent over one trillion dollars more every single year. It means that when (and not if) you throw another half a trillion to one trillion dollars on top of their present budgetary house of cards, there is simply no way that it will possibly remain standing.

When the proverbial chips finally come falling down (as both the Bank of International Settlements and Congressional Budget Office are warning they eventually must), there simply will not be enough gold available to go around for everyone who is desperate to have some with which to protect their failing dollars, pounds, euros, and yen.

It means that now is the time to lock in your share of the yellow metal for the sake of your retirement accounts. Consider a Gold IRA and the IRA-approved gold coins and bullion while you can still afford history's greatest proven asset safeguarding hedge and protection. It is all too obvious why gold makes sense in an IRA.

Gold: $2,387.15

Gold: $2,387.15

Silver: $27.92

Silver: $27.92

Platinum: $931.02

Platinum: $931.02

Palladium: $903.43

Palladium: $903.43

Bitcoin: $67,910.26

Bitcoin: $67,910.26

Ethereum: $3,278.81

Ethereum: $3,278.81