- GOLD IRA

- Download Our 2024 Precious Metals IRA Investor’s Guide.

Click Here

Gold IRA

Gold IRA

- Investing

-

- CRYPTO IRA

- PRICES & STATS

- RETIREMENT PLANS

Questions? Call (888) 820 1042

Questions? Call (888) 820 1042

Silver

Silver Gold

Gold Platinum

Platinum Palladium

Palladium Bitcoin

Bitcoin Ethereum

EthereumAble Lending Review

Disclosure: Our content does not constitute financial advice. Speak to your financial advisor. We may earn money from companies reviewed. Learn more

Last Updated on: 25th March 2023, 12:41 am

Able Lending

- Phone : N/A

- URL :

- Global Rating

- Good

User Rating

- 0 No reviews yet!

Review Summary :

Small businesses that are tired of hitting their family and friends up for uncomfortable loans will be glad to have a structured platform for doing it and paying fair interest to their backers now. The 3:1 matching service of Able ensures that businesses with a reasonable number of from three to five believers in their product or service will be able to get a small business loan at a good interest rate of from 8% to 16%, assuming they pass underwriting standards and agree to the 3% loan origination fee.

Pros:

- The platform takes care of all processes and details of repayment for the borrowers via monthly ACH withdrawals from the borrowers' same account to which it deposited the loan funds and also disburses interest payments to all investors in question.

- No prepayment penalties for paying back the loan earlier than the maturity date.

- Account origination fees are the only additional fees besides the interest rate, and these are a low 3% one time charge.

- Because borrowers bring onboard their own known investors for a quarter of the loan, rates are able to be provided at significantly lower than traditional lenders' rates and even rival P2P platform rates at typically from 8% to 16% maximum.

Cons:

- Investors lose 100% of investment in the event of any type or time of default by their underlying borrower.

- The safety policy statement goes a long way to unnerving potential investors and borrowers alike.

Quick Facts about Able Lending

Reviewed By:David Crowder

Have you purchased products from Able Lending? Leave a review!

(Please note: Able Lending's webpage is currently inactive, and the business may be defunct. For more reviews, consider browsing our list of the top 10 gold IRA companies in America.)

The element that makes this industry so very exciting is that there is always something new, or some new angle, in the Peer to Peer Lending and Crowdfunding space. Able Lending is a P2P outfit whose own angle is that it is the very first collaborative lender in the small business loan world. Read on to learn how you can get involved as an investor or a business borrower in this interesting collaborative opportunity.

Able Lending Intro & Background

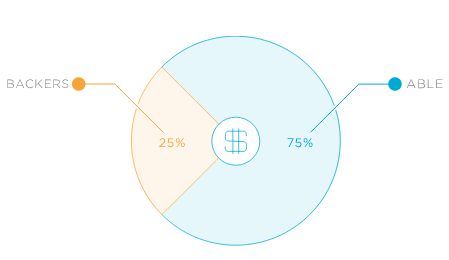

Able Lending has its own unique angle on Peer to Peer Lending. They want you all in on your small business loan. They will cheerfully reward you for this minor inconvenience by offering you a very competitive rate of starting at 8% only for bringing in between three and five of your own investors who must contribute 25% of the funds for your loan between them. Once you have met your part of the collaborative arrangement, Able promises to deliver the remaining 75% of the funding to you.

Able Lending Founder and Management Team

Co-Founder Will Davis got his MBA from Harvard Business School. He has written U.S. Congressional financial legislation focusing on monetary and banking policy. He has also testified before Congress on public policy and innovation issues in the past.

Co-Founder Evan Baehr has worked side by side with some of the foremost creators and leading idea-makers of our time, such as Facebook's Sheryl Sandberg, PayPal's Peter Thiel, and similar leaders when he served at the White House and on Capitol Hill. He is also a Harvard Business School MBA who graduated magna cum laude from Princeton and Yale.

Able Lending Loans

Because borrowers are forced to deliver between three and five of their own investors at 25% of the funding needs, Able Lending is able to provide among the lowest interest rates on the market. The investors themselves serve as a form of business reference. Able is then confident enough to provide the remainder 75% of the funding at interest rates that range from 8% to 16%. Loan dollar amounts start at $25,000 and go on up to $500,000.

How Able Lending Works

Able is different from many of its P2P and crowdfunding rivals in that it actually operates legally in every state in the country. Their angle of making prospective business borrowers find between three and five backers puts a lot of onus on the business owners. The backers have to pledge and deliver at least $1,000 each so that the backers' combined contribution reaches at least 25% of the total requested loan dollar amount. On top of this, no single borrower is allowed to fund more than 50% of the total capital contribution. The borrower is then funded the rest of the money by Able, which signs clearly defined loan agreements between Able and the borrower.

The backers' accounts are then debited and Able matches them at the 3:1 ratio to fund the borrower's loan. As the borrower repays the loan, Able makes interest deposits to your investment bank account every month until the end of the loan term. At the end of this term, you finally get your principal back, unless of course the loan defaults. In the event of a loan default, all of your principal is lost, as Able has absolute seniority on any loan. You get to keep your interest payments that you have received up to that point, but lose 100% of everything else.

In order to qualify for these loans, borrowing businesses must have been operational for minimally six months, have a verifiable yearly revenue of minimally $50,000, and possess a substantial social media business presence. The borrower has to fill in the online profile which covers the business information and what the loan is needed to help fund. It takes Able less than 24 hours to respond with a list of particular documents that they require from the business. After these are provided, credit checks on the business owners are completed so that decisions on the underwriting success are delivered in no more than three business days.

Backers are in the interesting position of choosing their own interest rate. They can charge as high as the rate that Able is getting, from 8% to 16%, or they can go lower by as much as half of Abel's rate. It is only in the final quarter of the term of the loan when Able feels confident enough in the borrower repaying that they will begin to return the principal amount to the backers. Backers are also not only limited to the one small business loan project at a time. They may fund up to five different businesses each year via the Able Lending platform.

Able Lending Services

- Loan Matching Service – The backers unlock 3/4's of the funding from Able by contributing their 25% total. Able then matches the remaining 75% of the borrower's loan.

- Repayment Servicing – Able's platform handles the repayment of the loan. This is how they provide legality and structure to the family and friends model of lending.

- Ask Able Free Service – We are so impressed with this free service, arguably the best feature of the entire Able Lending platform. They say that they love helping entrepreneurs grow, and this is why they offer thirty minute no charge phone calls to help answer any and all relevant small business questions you may have, and they do this totally for free. The way these calls work is that you first book an appointment for a free 30 minute phone call. This includes 10 minutes for introductions and overview, 10 minutes for your questions, and 10 minutes for Able Lending's advice and recommendations to help your business surpass its prior results and to flourish in the future.

- Able 100 Network – This represents a new group of committed small business owners who fund each others' growth via collaborative loans. It is more like a community that cares than a more elite and smaller lending network within the lending network. Companies within this group have already fundraised even millions of dollars so far.

- Higher Investor Returns – The returns that Able pays are considerably better than your typical savings accounts or CDs.

- Awkwardness Avoided – You will never need to start an uncomfortable family conversation pertaining to loans or money again.

Able Lending Locations

Able has a single office based in Austin, Texas. Their corporate headquarters is found at 503 Colorado Street, Suite 500, Austin, Texas 78701.

Able Lending Interface Screenshots

Able Lending Safety

It is important for you to know before you invest that in the event of a borrower default, you will receive nothing from your principal back, regardless of how much of the loan has been repaid before the default occurs. The rationale behind this draconian policy is that Able has seniority over all backers in the scheme of the loan, meaning all backers are subordinate to them. Backers will only be allowed to keep the interest they have been paid to that point in the event of a default.

Regarding privacy, Able values its users and visitors privacy. They make it their priority to safeguard any information that might be identifiable personally from any of their clients or users.

As far as safeguarding personal and financial data goes, Able discloses that they employ a variety of technical, managerial, and physical safeties to protect your personal information's security. At the same time, they take great pains to disclose to you that they can not guarantee the safety of any information you transmit to them, and that you are doing this at your own personal risk. They promise to go through all reasonable commercial efforts to secure their systems.

But they again state that they will not and can not guarantee that your information will not be stolen, altered, or destroyed by any invasion by hackers of their technical, physical, and managerial safeties. We can understand where they are coming from in trying to cover themselves against future potential failures and lawsuits, but it is not at all reassuring for either investors or borrowers to hear repeated a number of times that nothing can assure the safety of their personal and financial data put up on the platform. This is especially true when you consider what a total nightmare it is if and when your financial or personal information is compromised.

Able Lending Complaints and Ratings

The Better Business Bureau maintains its highly desired A+ rating on Able Lending. BBB also states that Able fully meets its rigorous accreditation standards that include, among other things, their commitment to do their very best in good faith to resolve any and all complaints from customers. They hold this longed-for ranking because of the number of years that the business has been running, and the fact that they have zero complaints lodged against them with the BBB.

Able Lending Customer Support

Able is free enough with its phone number and email address that users are told to contact if and when they require customer support. The website itself leaves a lot to be desired for effective online customer support, as it is not very transparent and is sketchy on critical company information at points. They do provide live chat, which helps to make up for this. Very few of the Peer to Peer Lenders and Crowdfunding sites are offering all three means of customer support with phone, email, and live chat contact these days.

Able Lending Costs & Fees

Able starts its interest rates at 8% and has a range on up to 16% for borrowers, depending on their qualifications and especially credit rating, amount of loan, and length of repayment term. Lower interest rates are awarded for shorter payoff terms in the one to five years repayment scheme possibilities from which borrowers must choose. There is also an upfront, single time origination fee charge of 3% for managing the loan. This is one of the lower origination fees in the small business loan P2P space. Pre-paying the loan does not incur any additional costs or fees. Investing backers do not pay anything to sign up, register for, or back any loans on the platform.

Final Words on Able Lending

Able Lending is the one and only outfit that we have heard of that is practicing this form of collaborative lending, whether to small businesses or individuals. This makes them truly unique in the P2P and Crowdfunding space. It also is a discouraging step that borrowers have to think over seriously before they invest their time and reputation into attempting to bring on board from three to five different backers who must pre-fund 25% of the hoped and anticipated for loan amount. Investors will not be thrilled about the subordination of their defaulting loan claims to Able that mean de facto all principal is lost in the event of any type of default, regardless of whether it happens in the first quarter of the loan's life or in the last quarter. Investors and borrowers alike will likely have some issue with the admission that no transfer of data and personal and financial information is considered to be foolproof safe with and by Able.

Able Lending

- Phone : N/A

- URL :

- Global Rating

- Good

User Rating

- 0 No reviews yet!

Review Summary :

Small businesses that are tired of hitting their family and friends up for uncomfortable loans will be glad to have a structured platform for doing it and paying fair interest to their backers now. The 3:1 matching service of Able ensures that businesses with a reasonable number of from three to five believers in their product or service will be able to get a small business loan at a good interest rate of from 8% to 16%, assuming they pass underwriting standards and agree to the 3% loan origination fee.

Have you purchased products from Able Lending? Leave a review!

Gold: $2,387.15

Gold: $2,387.15

Silver: $27.92

Silver: $27.92

Platinum: $931.02

Platinum: $931.02

Palladium: $903.43

Palladium: $903.43

Bitcoin: $67,910.26

Bitcoin: $67,910.26

Ethereum: $3,278.81

Ethereum: $3,278.81