- GOLD IRA

- Download Our 2024 Precious Metals IRA Investor’s Guide.

Click Here

Gold IRA

Gold IRA

- Investing

-

- CRYPTO IRA

- PRICES & STATS

- RETIREMENT PLANS

Questions? Call (888) 820 1042

Questions? Call (888) 820 1042

Silver

Silver Gold

Gold Platinum

Platinum Palladium

Palladium Bitcoin

Bitcoin Ethereum

Ethereum4 Big Mistakes to Avoid In Retirement Planning

Disclosure: Our content does not constitute financial advice. Speak to your financial advisor. We may earn money from companies reviewed. Learn more

Last Updated on: 29th November 2015, 03:14 pm

Mistake #1 Underestimating Cost of Living

To be able to plan for retirement you need to have a good estimate of what your living costs will be once you stop working. This is necessary to be able to come up with a number when you ask yourself how much will I need to retire?

Most people in the early stages of retirement planning do not have a clear idea of how much they will need. Some advisors suggest 80% of your income is the correct target for calculating your retirement needs. That would seem very arbitrary to me, as it will depend on how much your life style is going to change after retiring.

Overestimating may give you the sensation that the sum you need is unachievable and create frustration. Underestimating may mean that you might find yourself needing to make a series of cut backs to manage with what you have. There are plenty of online retirement calculators. The one from Kiplinger takes into account your social security contributions as well as current pension savings and considers the equity you may release by selling your home.

Mistake #2 Not Making Sufficient Provision for Health Care Costs

For a lot of people thinking of the possibility of not being in good health doesn’t appeal much. But we are liable to the possibility at some point. As we get older that possibility becomes greater. Yet not planning for higher health care costs is a common mistake.

Many presume Medicare will cover all costs, that is simply not the case. Some reports show that a healthy couple of 55 years of age retiring in 10 years may need on average $463,849 to cover lifetime health care costs. You have to think that apart from costs not covered by Medicare there will also be dental, co-pays and other out-of-pockets to take into account.

We also need to consider that most health care costs will occur later on in retirement, as in general we are aging better. But this means we have to be aware and make provisions for extra expenses much later on.

Mistake #3 Saving Later Rather Than Sooner

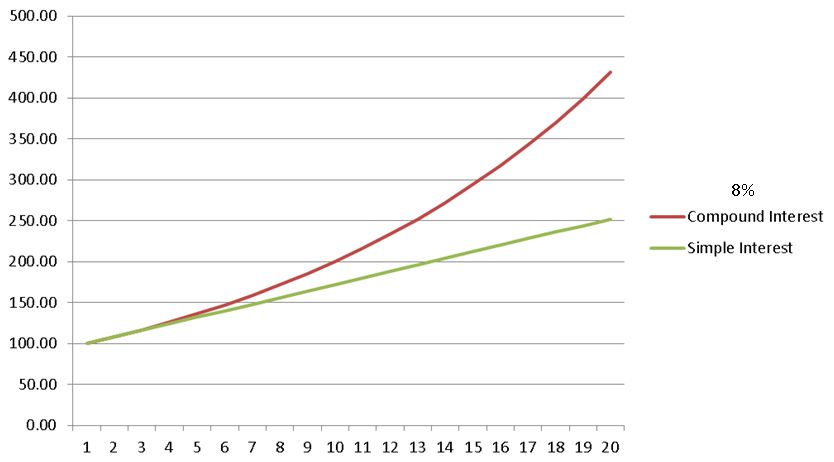

This is paramount to being successful in reaching your retirement goals. The effect of compounding interest plays a very important role when we start saving early on. Like Einstein said “Compound interest is the eighth wonder of the world, he who understands it earns it, he who doesn’t pays it”

The effects of compounded interest over long periods of time can be clearly seen by taking an example. Let’s say a 25 year old has a $1 million retirement target, by saving $345 a month, assuming the investment earns 8% a year, this person would have to save for 20 years to reach his/her goal. This is the effect of earning interest on interest, after 20 years saving $345 per month the retirement nest egg would be $204,727. After the next 20 years without any further contributions, other than the interest earned, that amount would increase to over $1 million.

Whereas a 45 year old would need to save $1,698 per month for 20 years to reach the same goal.

Those saving goals may not necessarily be within the reach of every younger or older person. However the idea is to save a percentage of your earnings per year on a consistent basis, and above all never touch the interest being earned or the capital itself.

Mistake #4 Not Revising your Retirement Plan Regularly

Your retirement planning should be revised regularly, on a yearly basis. Some advisors suggest revisiting your retirement plan every 3 to 5 years. I say that may not be enough as many changes could have happened precisely in the previous year. Why would you wait to revise your finances for retirement 3 or 5 years later.

Having in mind to re-think about your retirement planning makes sure you’re pension scheme is up to date and relevant. Many things can change in the market place from one year to the next. It may not be so appealing to hold a large portion of your retirement money in stocks at some point and other assets may be more appropriate.

Changes to your lifestyle or income may have recently occurred. Your spouse may have received a promotion and salary raise, your in-law may have moved in with you, or any other series of events. In this case your current retirement plan is probably out of date and not in line with your current needs and possibilities.

Gold: $2,387.15

Gold: $2,387.15

Silver: $27.92

Silver: $27.92

Platinum: $931.67

Platinum: $931.67

Palladium: $903.43

Palladium: $903.43

Bitcoin: $67,909.13

Bitcoin: $67,909.13

Ethereum: $3,254.68

Ethereum: $3,254.68