Silver

Silver Gold

Gold Platinum

Platinum Palladium

Palladium Bitcoin

Bitcoin Ethereum

EthereumThe Debt Ceiling Crisis: What it Means for Gold Investors

Disclosure: We are reader-supported. If you purchase from a link on our site, we may earn a commission. Learn more

Last Updated on: 14th December 2025, 12:08 am

Updated & Edited: December 2025

Debt ceiling headlines tend to show up fast, feel dramatic, and then disappear once Congress acts. Still, the drama is not harmless. Even getting close to the “X-date” can rattle markets, push short-term rates around, and create a risk-off mood that retirement investors feel in their accounts.

Free 2026 Gold Investment Kit (Noble Gold)

If you’re considering physical gold for diversification, this kit helps you understand the basics, the common pitfalls, and the questions to ask before moving retirement money.

Disclosure: If you request information through the link above, we may earn a referral fee. This does not affect our editorial opinions.

This article updates our original 2023 debt ceiling coverage so it reflects what actually happened, where things stand now, and what to watch the next time Washington plays chicken with the borrowing limit.

Table of Contents

- Where the debt ceiling stands now (quick 60-second version)

- What is the U.S. debt ceiling?

- Debt ceiling vs. government shutdown (they get confused a lot)

- Debt ceiling 2023: what actually happened

- Why gold investors pay attention to debt ceiling episodes

- What to watch the next time the debt ceiling becomes “urgent”

- 👍 Pros and 👎 Cons for gold investors during debt ceiling drama

- How retirement investors can prepare without panic

- Bottom line

Where the debt ceiling stands now (quick 60-second version)

- The 2023 standoff ended: The Fiscal Responsibility Act was signed on June 3, 2023 and suspended the debt limit through January 1, 2025. (White House bill summary)

- The limit was reinstated in early 2025: On January 2, 2025, the debt limit was reinstated at about $36.1 trillion and Treasury prepared to use “extraordinary measures.” (Treasury letter, Congressional Research Service)

- Congress raised it again in mid-2025: A reconciliation law enacted on July 4, 2025 raised the debt limit by $5 trillion to $41.1 trillion. (CRS, CRS In Focus)

So the “June 5, 2023 deadline” you may remember was part of the old coverage. It did not end in default. Congress acted before Treasury ran out of room.

What is the U.S. debt ceiling?

The debt limit (or “debt ceiling”) is a legal cap on how much the U.S. Treasury is allowed to borrow to meet obligations that have already been authorized by law, like Social Security benefits, Medicare payments, military salaries, interest on Treasury bonds, tax refunds, and more.

Important nuance: the debt ceiling does not authorize new spending. It’s about financing commitments that already exist. Treasury’s plain-English explanation is worth reading if you want the cleanest definition: U.S. Treasury: Debt Limit.

Debt ceiling vs. government shutdown (they get confused a lot)

A government shutdown happens when Congress fails to pass appropriations to fund parts of the government. A debt ceiling breach happens when Treasury can’t borrow to pay bills the government already owes. They can happen around the same time, but they are not the same problem.

If you want a solid explainer from a reputable source, Brookings has a clear breakdown here: Shutdown vs. debt ceiling: what’s the difference?

Debt ceiling 2023: what actually happened

In spring 2023, markets were focused on the “X-date,” the point where Treasury would run out of cash and accounting maneuvers (called “extraordinary measures”) to keep paying bills on time.

The standoff ended when the Fiscal Responsibility Act of 2023 became law on June 3, 2023, suspending the debt limit through January 1, 2025. That removed default risk for that cycle, but it did not make the debt ceiling issue go away forever. (White House)

The cost of getting close to default

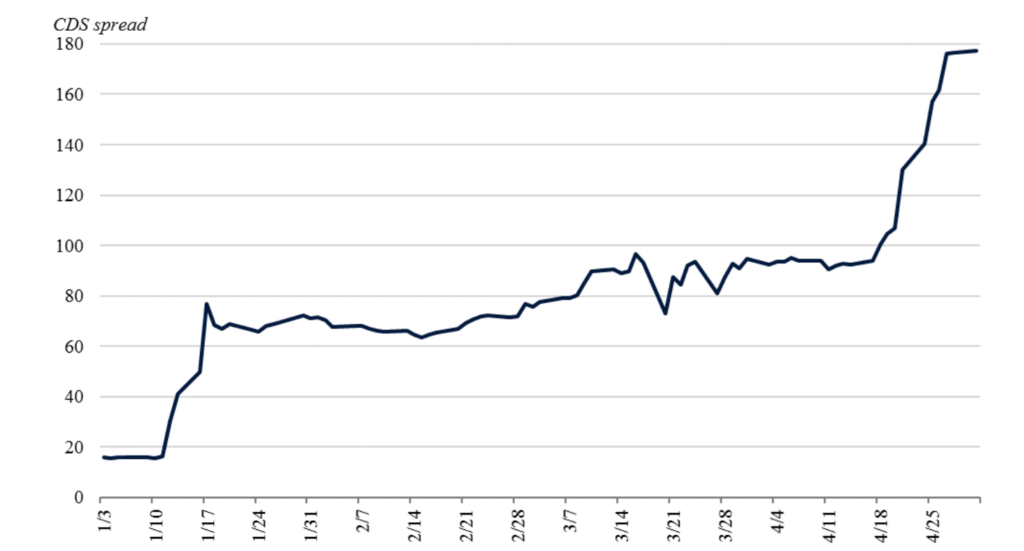

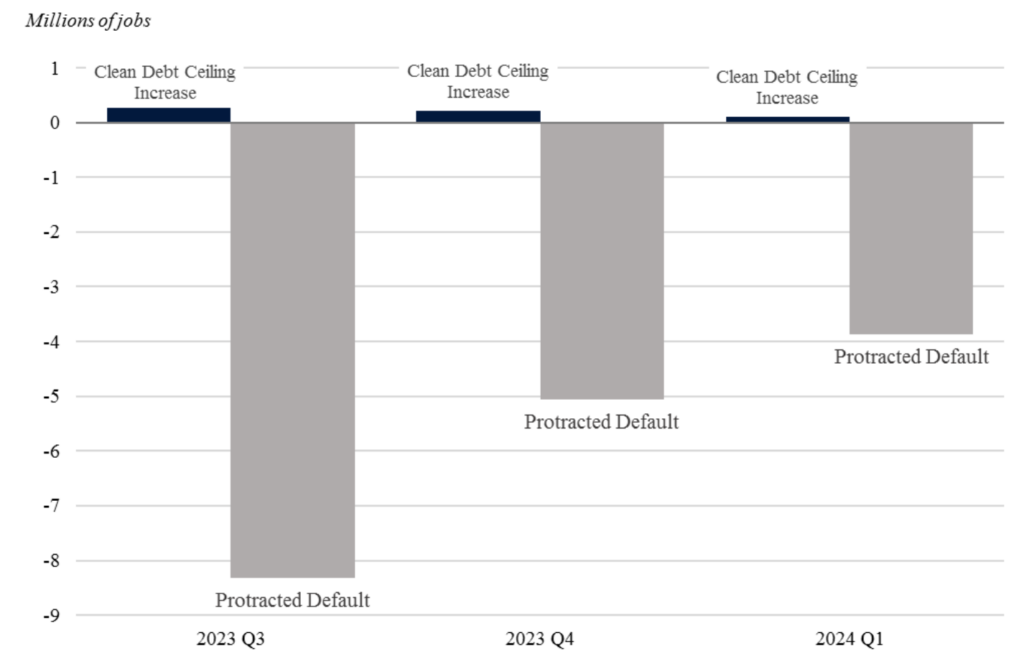

One reason investors take these episodes seriously is that the downside scenarios are ugly. In May 2023, the White House Council of Economic Advisers published scenario analysis showing a protracted debt ceiling breach could trigger a sharp recession and a major stock market drop. You can read the analysis here: CEA: Debt ceiling scenarios (May 2023).

Image 1: One-year U.S. government bond insurance premiums (Source: White House CEA)

A key takeaway is not “this exact chart will repeat.” It’s that debt ceiling brinkmanship can distort markets even if a deal arrives at the last minute.

Image 2: Job gains/losses under default or clean debt ceiling increase scenarios, Q3 2023 to Q1 2024 (Source: White House CEA)

Why gold investors pay attention to debt ceiling episodes

When default risk enters the conversation, investors tend to do some version of: reduce risk, raise liquidity, and look for assets that historically hold up better during chaos. That is why gold gets discussed alongside things like cash, short-term Treasuries, and defensive equity positioning.

Two practical reminders for real-world investors:

- Gold can hedge stress, but it’s not magic: in liquidity crunches, gold can wobble right along with everything else before it finds its footing.

- Owning gold has “plumbing”: storage, spreads, taxes, and the structure you use (taxable vs. IRA) matter just as much as the headline price.

If you want a quick refresher on pricing mechanics (and why headlines about “spot” can be confusing), this guide helps: our spot price explainer.

And if you’re thinking about gold primarily as a “crisis hedge,” this older piece still frames the psychology well: why gold is often treated as a safe haven.

Want the “plain English” version of adding gold to a retirement account?

Noble Gold’s free 2026 kit walks through the basics and the questions to ask before doing a rollover.

Get the free kit here (Disclosure: we may earn a referral fee.)

What to watch the next time the debt ceiling becomes “urgent”

These are the signals I personally watch during debt ceiling cycles, because they’re more useful than cable-news panic:

- Treasury updates on extraordinary measures: Treasury often sends letters explaining timing and cash constraints. (Example: Yellen’s debt limit letter.)

- Short-term Treasury bill yields: stress often shows up first in very short maturities around key dates.

- Credit rating pressure: even “near misses” can cause reputational and market damage. In 2025, Moody’s downgraded the U.S. rating citing rising debt and deficits. (Coverage: Reuters.)

- Broad risk sentiment: widening credit spreads, volatility indexes, and rushed “de-risking” behavior.

👍 Pros and 👎 Cons for gold investors during debt ceiling drama

👍 Pros

- Portfolio ballast: gold often behaves differently than equities when investors are nervous, which can smooth out volatility.

- No counterparty risk for physical bullion: a bar is a bar, regardless of which institution looks shaky that week.

- Compact value storage: you can hold meaningful value in a relatively small footprint (especially compared to many other “hard assets”).

👎 Cons

- Short-term whiplash is real: in a true liquidity rush, gold can dip before it rebounds.

- Costs matter: spreads, storage, shipping, and IRA fees can quietly eat performance.

- It’s not an “all in” solution: gold is usually best as a slice of a broader plan, not the whole plan.

How retirement investors can prepare without panic

If the debt ceiling becomes front-page news again, you don’t need to flip your life upside down. A few reasonable steps usually beat emotional trading:

- Re-check your diversification: if you want examples of how people blend metals with traditional holdings, see these portfolio breakdowns.

- Know your “how” before you move money: if you are considering metals in an IRA, understand rollovers first: this rollover guide is a good starting point.

- Use the right account type: for many investors, the key is simply learning what a self-directed IRA can and cannot hold: self-directed IRA basics.

- Choose reputable providers and policies: fees, depository storage, and buyback terms matter. Start with our gold IRA company list and compare the details.

- If you own metals outside an IRA: think through practical storage and insurance. This checklist can help: home storage guide.

The 14th Amendment and the “can the President bypass Congress?” question

Every time the debt ceiling gets tight, someone raises the Fourteenth Amendment (Section 4) and asks whether the executive branch could sidestep Congress. The short answer is: it remains legally disputed, it has not been decisively tested at the Supreme Court level in a modern debt ceiling breach, and it would likely trigger years of litigation and market uncertainty if attempted.

If you want the exact language, the official text is here: U.S. Constitution, 14th Amendment, Section 4.

Bottom line

The debt ceiling is one of those Washington mechanics that looks “procedural” until it isn’t. The 2023 episode was resolved, the ceiling was reinstated in early 2025, and Congress raised it again in July 2025. The next showdown will likely come later, but the playbook is the same: markets hate uncertainty, and retirement investors do best when they prepare calmly instead of reacting emotionally.

Disclaimer: This article is for informational purposes only and is not financial advice. Always do your own research and consult a qualified professional before making investment decisions.

Gold: $4,052.89

Gold: $4,052.89

Silver: $58.17

Silver: $58.17

Platinum: $1,594.04

Platinum: $1,594.04

Palladium: $1,245.52

Palladium: $1,245.52

Bitcoin: $64,236.44

Bitcoin: $64,236.44

Ethereum: $1,871.30

Ethereum: $1,871.30